Falcor/E+ via Getty Images

The Q1 Earnings Season for the Gold Miners Index (GDX) has ended, and the shining stars were the royalty/streaming companies. This was evidenced by them maintaining their exceptional margins while most producers struggled to hold the line, and some smaller names have become un-investable due to cost increases. Royal Gold (NASDAQ:RGLD) was one of the shining stars in Q1, reporting consistent growth in revenue and operating cash flow, with multiple positive developments across its portfolio. Given Royal Gold’s inflation-protected business model and a favorable landscape for deal-making, I would view any sharp pullbacks as buying opportunities.

Andacollo Mine (Company Website)

Royal Gold released its Q1 results last month, reporting quarterly production volume of ~86,500 gold-equivalent ounces [GEOs], a 9% increase from the year-ago period. This was driven by higher sales at principal assets like Mount Milligan, Andacollo, and Cortez, plus contributions from newly acquired royalty/stream assets (Red Chris – Canada, NX Gold Mine – Brazil). In addition, while a slow ramp-up has affected revenue, the newly constructed Khoemacau Copper Mine contributed to just over 1% of quarterly revenue. Let’s take a closer look below:

Q1 GEO Volumes And Revenue Per Asset

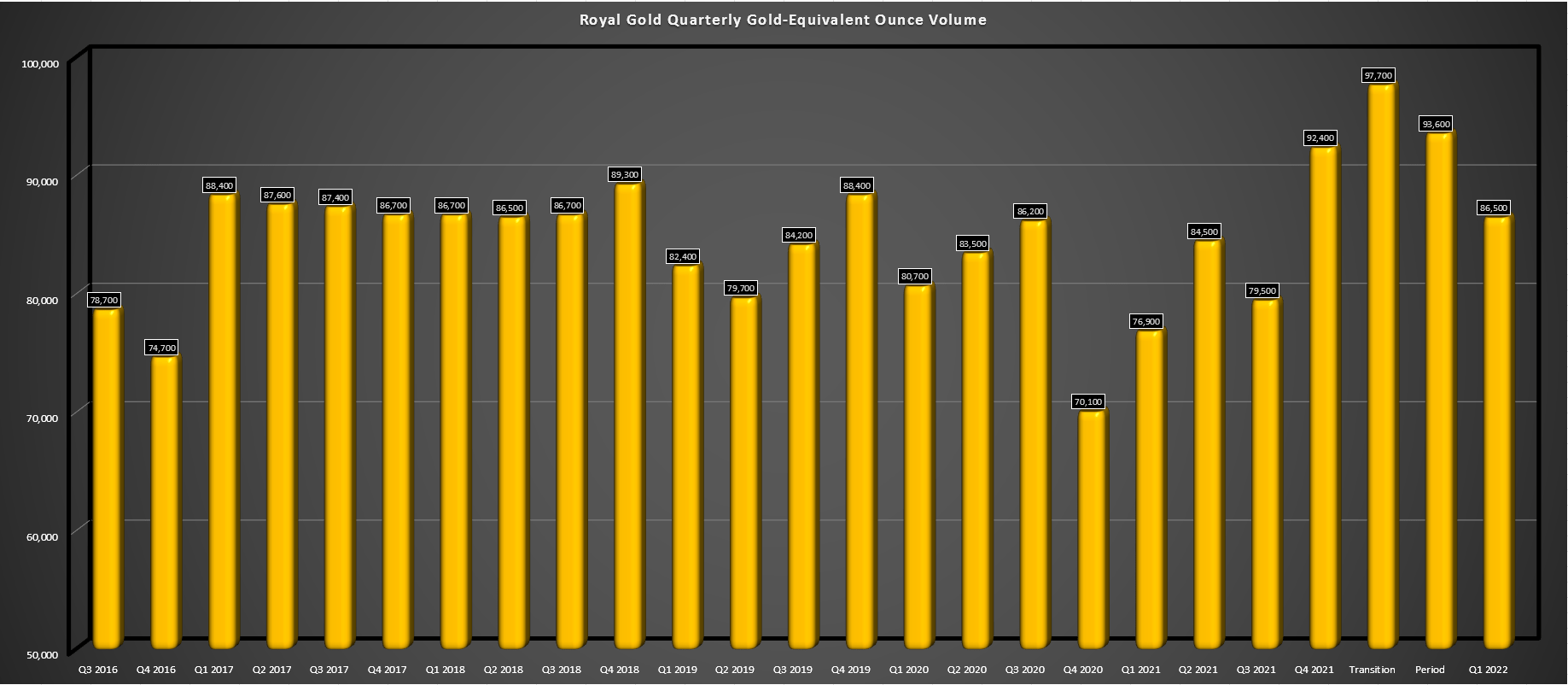

Royal Gold – Quarterly Gold-Equivalent Ounce Volume (Company Filings, Author’s Chart)

Looking at the chart above, Royal Gold has seen limited growth in GEO volumes over the past few years (2017-2020), given that it had a quieter period for deal-making, and its major investment had yet to begin production (Khoemacau). However, with Khoemacau now online with a higher stream rate (100% of payable silver) and a busy year for deals in 2021, Royal Gold is set to return to growth in a big way. We’ve seen evidence of this in the past few quarters, with GEO volumes hitting a new record in calendar year Q3 2021 (97,700 GEOs), increasing by more than 10% in calendar year Q4 2021, and then inching up by 9% in Q1 2022.

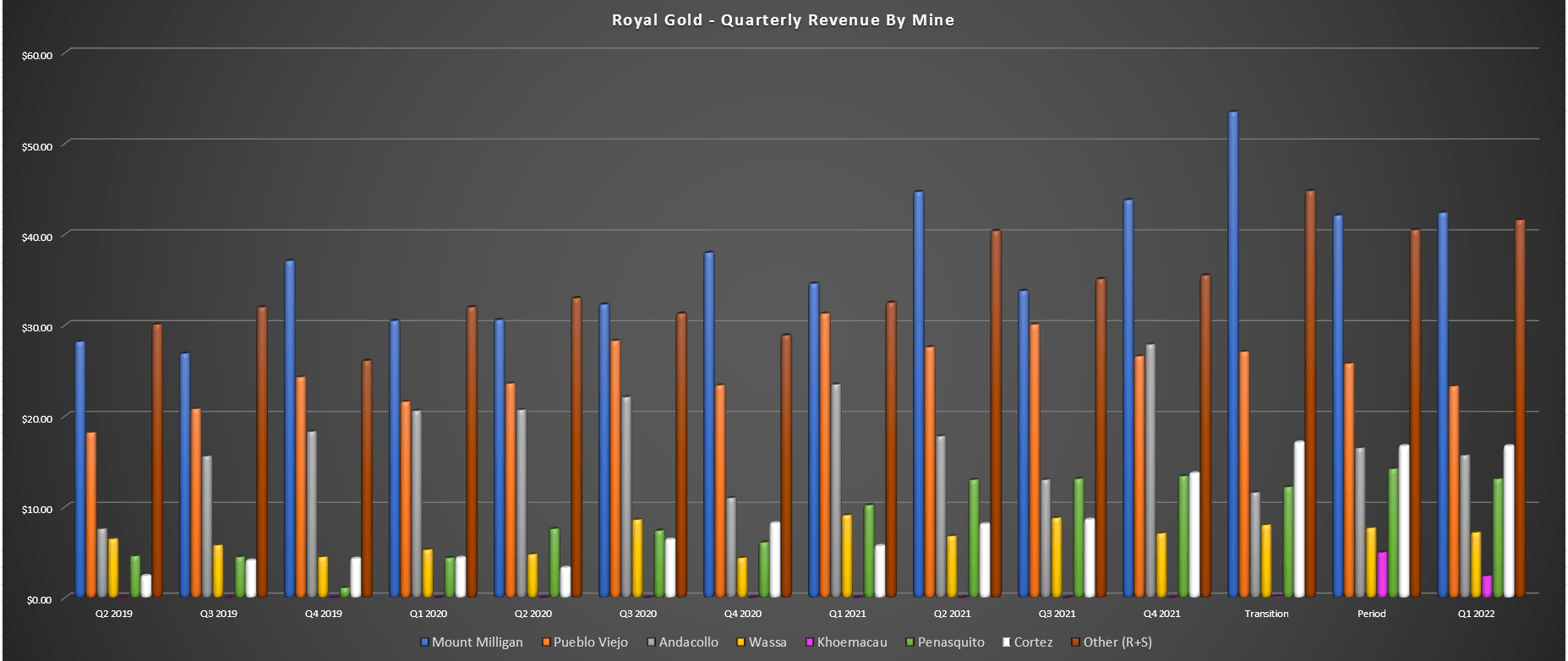

Royal Gold – Quarterly Revenue by Mine (Company Filings, Author’s Chart)

Digging into the assets a little closer, most of the company’s larger assets contributed higher revenue on a year-over-year basis. For example, revenue was up to $42.4 million at Mount Milligan (Q1 2021: $33.8 million). Revenue increased to $9.1 million at Rainy River (Q1 2021: $8.8 million). Meanwhile, Royal Gold reported revenue of $15.7 million at Andacollo (Q1 2021: $13.0 million) and $16.7 million at Cortez (Q1 2021: $8.6 million). Finally, three new assets (two newly acquired, one that’s finally completed construction) contributed a total of $9.8 million in Q1 2022 (NX Gold, Red Chris, Khoemacau).

Medium-Term Growth

At Khoemacau, which will be a meaningful contributor in 2023, the stream rate has been increased to 100% of payable silver, and the ramp-up is seeing gradual progress. As of March, underground production had increased to 5,700 tonnes per day vs. 3,000 tonnes per day in January, nearly 60% of the way to the 10,000-tonne full run rate. The plan is to see this production level reached in Q4 of this year, setting Royal Gold for a record year in 2023 from a revenue and cash flow standpoint. This is because, even at a $22.00/oz silver price, Khoemacau will contribute ~$33 million in revenue after the 20% of spot price, or ~$41 million in revenue at a $27.00/oz silver price.

Khoemacau Copper Mine (Khoemacau Copper Presentation)

According to Khoemacau Copper, there is the potential to increase production significantly later this decade by bringing new mines online to feed the Boseto Processing Plant and directing Zone 5 production tonnes to a 4.5 million tonne per annum Processing Plant at Zone 5. If successful, this could double copper and silver production at the asset, translating to a significant lift in NPV (5%) at Khoemacau for Royal Gold with higher production in the earlier years. For those unfamiliar, Royal Gold is entitled to a 100% silver stream until 40 million ounces have been delivered, and production potentially increasing to ~3.5+ million ounces per annum later this decade vs. ~1.9 million would provide a meaningful boost to Royal Gold’s annual revenue and cash flow.

Khoemacau Copper – Expansion Potential (Khoemacau Copper Presentation)

Elsewhere in Royal Gold’s portfolio, the company will enjoy meaningful growth over the next few years from several smaller assets. These include:

- a 1% net smelter return [NSR] royalty at Cote Gold (attributable to ~70% of reserves)

- the potential for higher gold production at the NX Gold Mine which saw a 25% increase in reserves, and has excess capacity at the mill

- the King of the Hills Mine (1.5% NSR royalty), which poured its first gold last month

- the Bellevue Gold Mine in Australia (2.0% NSR royalty), which should head into commercial production within 18 months.

Sabina Gold & Silver – Goose Project (Sabina Gold & Silver Presentation)

Moving over to the Americas, Hochschild Mining (OTCQX:HCHDF) hopes to bring Mara Rosa into production in 2024, and Manh Choh ore production (which will be trucked to the operating Fort Knox Mill is planned for 2025. Finally, not only is Sabina Gold & Silver (OTCQX:SGSVF) financed for construction and has a date for planned production (Q2 2025), but it’s accelerating the expansion of its Goose Mill from 3,000 tonnes per day to 4,000 tonnes per day. Previously, the mill was set to operate at 3,000 tonnes per day with an expansion in Year 2.

Goose Project – Production Schedule (Sabina Technical Report)

Under the new plan, Sabina will construct the mill with a capacity of 4,000 tonnes per day to start, bringing forward some ounces, leading to slightly higher production earlier in the mine life. This should push annual production well over 300,000 ounces in the first two years of the mine life (Q3 2026 – Q3 2028), an improvement from ~272,000 ounces previously and a nice boost to Royal Gold’s revenue given its 1.95% gross smelter return [GSR] at Goose and 2.35% GSR at George. Like Khoemacau, there is longer-term expansion potential, with the possibility that Sabina could look at trucking ore from George at some point with its soon-to-be-mine permitted for up to 6,000 tonnes per day of capacity.

While none of these opportunities (Mara Rosa, Manh Choh, Goose, KOTH, Bellevue, NX Gold Expansion) are as significant as Khoemacau, they are meaningful contributors on a combined basis, and all of them are de-risked towards production. This is a major upgrade from the previous outlook, where there was little clarity on a production start date for Bellevue, Goose, or Mara Rosa. To summarize, while Royal Gold’s current GEO volumes may not highlight meaningful growth, the organic growth potential here cannot be understated, with the Red Chris Block Cave (OTCPK:NCMGF) being another massive opportunity post-2026.

Financial Results And Current Landscape

Looking at the company’s most recent financial results, revenue increased 14% year-over-year to $162.4 million, while quarterly earnings per share increased 18%, and operating cash flow improved to ~$101 million. This growth was attributed to higher GEO sales volumes, and higher average realized metal prices, with the gold price up 5% to $1,877/oz and the copper price up 17% to $4.53/lb. The only negative was the silver price, which makes up ~10% of revenue, that slid 9% to $24.01/oz in the period, and will be a further drag in Q2 2022.

Royal Gold – Quarterly Revenue (Company Filings, Author’s Chart)

The above results highlight why the royalty/streaming companies are so attractive within the gold sector, with higher margins across the board despite challenges for the sector as a whole and many other sectors. In terms of other sectors, some are seeing flat to lower margins year-over-year due to increased labor costs, commodity inflation, and supply chain headwinds. For gold producers, they’ve benefited from higher metal prices like Royal Gold, but this is partially offset by higher materials costs, higher labor costs, and inflationary pressures. However, due to Royal Gold’s business model, it’s been immune, and the outlook for its business is actually improving.

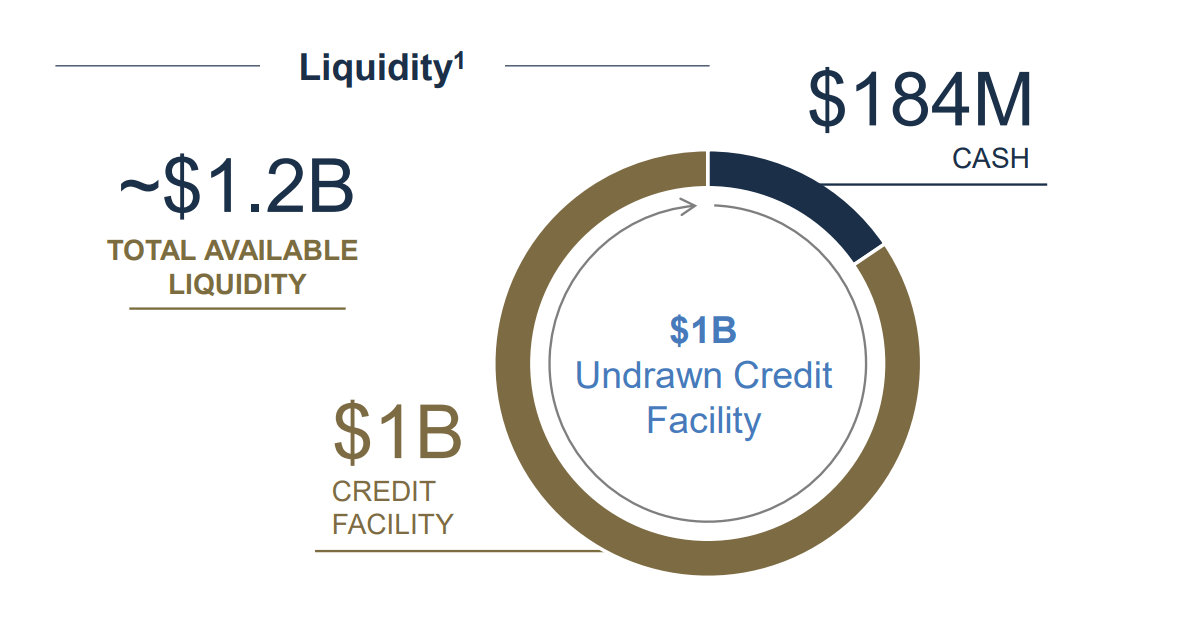

Royal Gold – Liquidity & Cash – March 2022 (Company Presentation)

This is because Royal Gold is sitting on ~$200 million in net cash and $1.2 billion in liquidity, providing lots of capacity for new deals without any share dilution. Simultaneously, many smaller producers are seeing cost overruns or struggling to finance previously planned expansions due to lower free cash flow generation (weaker margins). In addition, many development-stage companies will struggle to finance their projects without significant share dilution given that actual capex to build has increased, and there is less appetite for lending, or if there is appetite, it’s at higher rates. Faced with the choice of diluting shareholders to make up a funding shortfall with their share price 60% or more off its highs, a small stream/royalty is an attractive alternative for developers/producers.

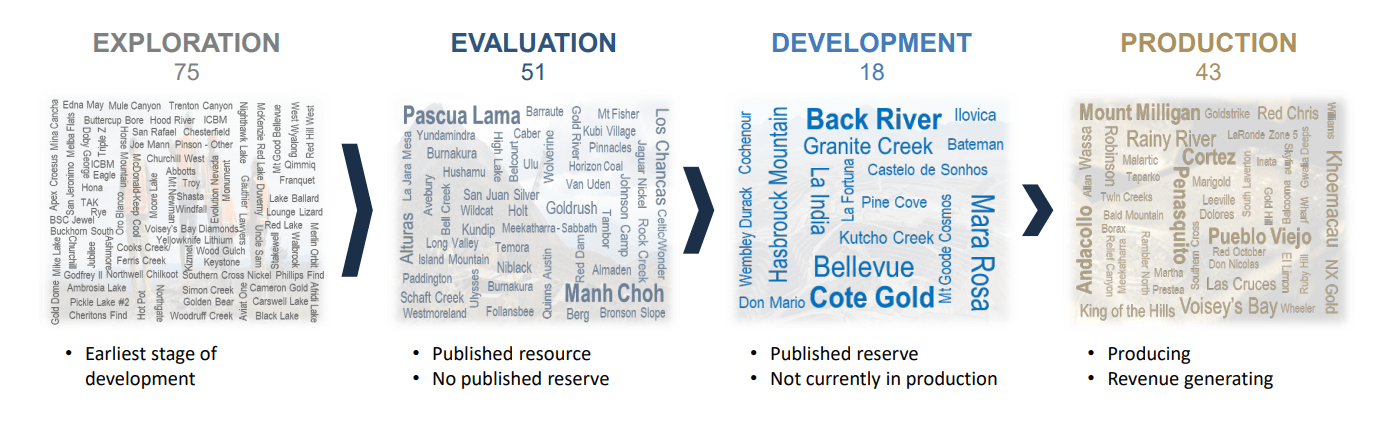

The same is true for gold/silver explorers. Many are seeing higher drilling costs, higher labor costs, and higher contractor costs and have also been pummeled due to the risk-off environment and less favorable outlook for the group. In the case of explorers, many are down 60-70% from their highs and would see double-digit share dilution if they tried to raise a meaningful amount of capital at these prices. As it stands, Royal Gold has 126 exploration/evaluation assets, and while it’s focused on development/production assets in recent deals, the changing dynamics could lead to a few more deals in this higher-risk, higher-reward segment of the sector.

Royal Gold Asset Portfolio (Company Presentation)

It’s important to note that more than 95% of early-stage projects will not become mines, and most explorers don’t make the cut. However, with even the best names being thrown out with the proverbial bathwater due to the poor sentiment, Royal Gold could have its pick of the litter among the top 1% of the most interesting projects that do have a good shot at one day becoming a mine. This is because these companies could look at selling a small stream or royalty to avoid share dilution at these levels.

In most cases or with a strong share price, share dilution would be preferable vs. limiting project upside with a stream/royalty. However, during a 60-70% off sale from a share price standpoint it’s a huge blow to dilute for these companies. Unfortunately, most explorers/developers don’t take advantage of the good times when they’re sitting at 52-week highs to raise more than enough capital, and it will cost them this time around, with Royal Gold being a potential beneficiary.

Valuation

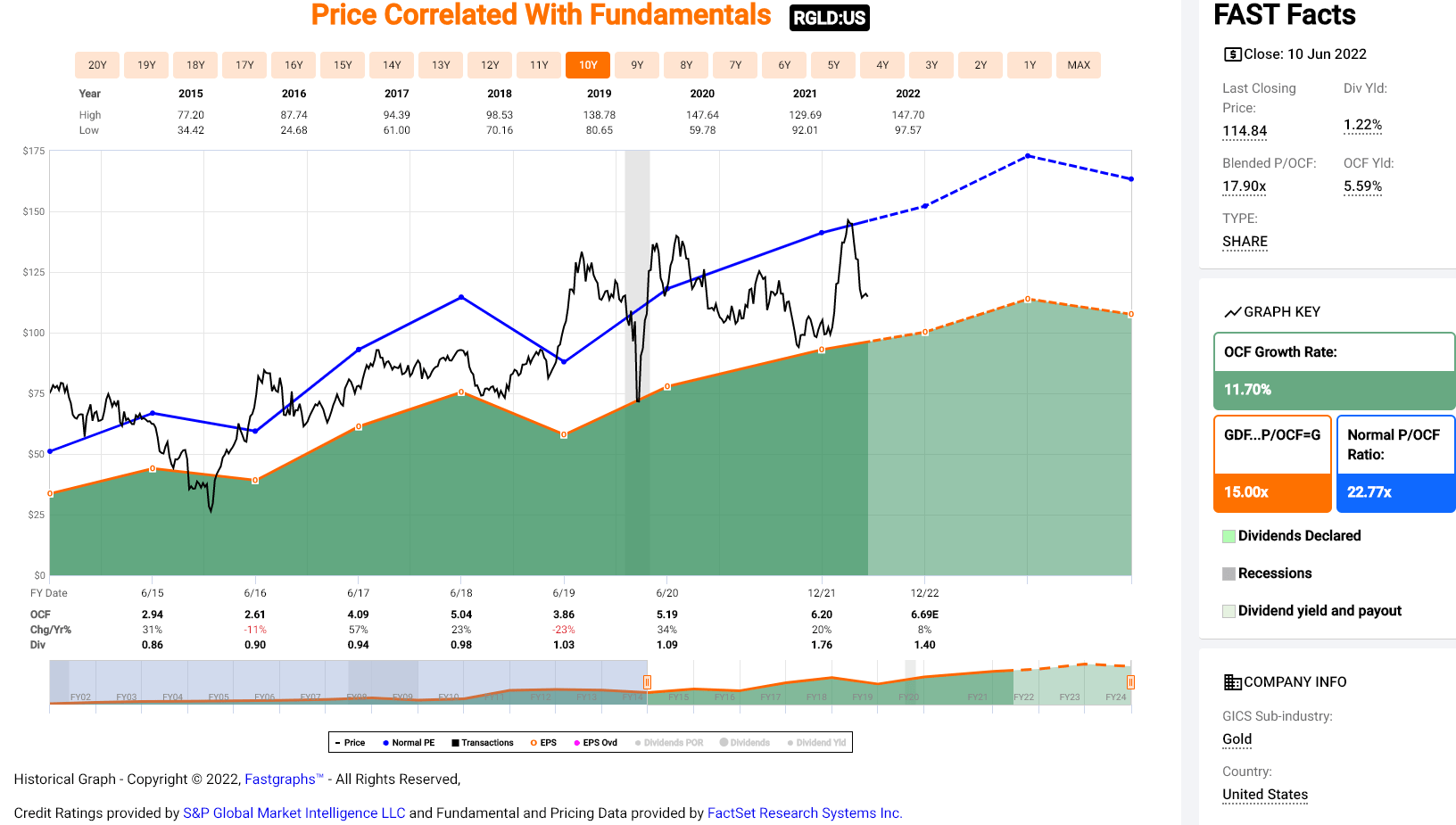

Looking at the chart below, we can see that Royal Gold has traded at an average cash flow multiple of ~22.8 over the past decade and currently trades at just ~15x FY2023 cash flow estimates, based on a conservative cash flow per share estimate of $7.80. Using a more conservative cash flow multiple of 20 for Royal Gold translates to a fair value of $156.00 per share for an 18-month price target. I would argue that this is a very conservative estimate, given that the gold price is at the high end of its 10-year range and the investment thesis for royalty/streamers vs. producers has rarely been better due to rising costs.

Royal Gold – Historical Cash Flow Multiple (FASTGraphs.com)

On a P/NAV basis, investors can get much more attractive valuations elsewhere in the sector and can buy companies at deep discounts to fair value, with developers trading at less than 0.50x, producers trading below 1.0x, and explorers trading at 0.30x net asset value. However, these discounted valuations reflect the risk in these investments, and in quite a few cases, these lower multiples are mostly justified. So, while some allocation to other areas of the sector makes sense given the discounts (assuming one focuses on the best companies), I would argue that Royal Gold is a staple for any precious metals portfolio with a growing dividend, a diverse asset base, and the fact that it’s inflation-resistant.

Penasquito Mine (Royal Gold Website)

Royal Gold reported a solid start to the year, and while Khoemacau might be a little behind schedule vs. initial plans, we will see meaningful growth from this asset in 2023. Besides, the positive developments across the portfolio have offset this, painting a bright future for Royal Gold as multiple assets come online and begin contributing between now and 2026. Given RGLD’s enviable organic growth profile, the improving landscape for deals, and its discipline to focus on only the best projects, further weakness in the stock should present a buying opportunity.