The semiconductor industry has long struggled with a notorious cycle of booms and nasty downturns. Now though, the industry is confident of beating the patterns of the past to extend what is an extraordinary run for the sector.

The industry, which reported a 26.2 per cent jump in sales to an all-time high of $555.9bn last year, wants to pour record-breaking sums into new fabrication plants, or fabs.

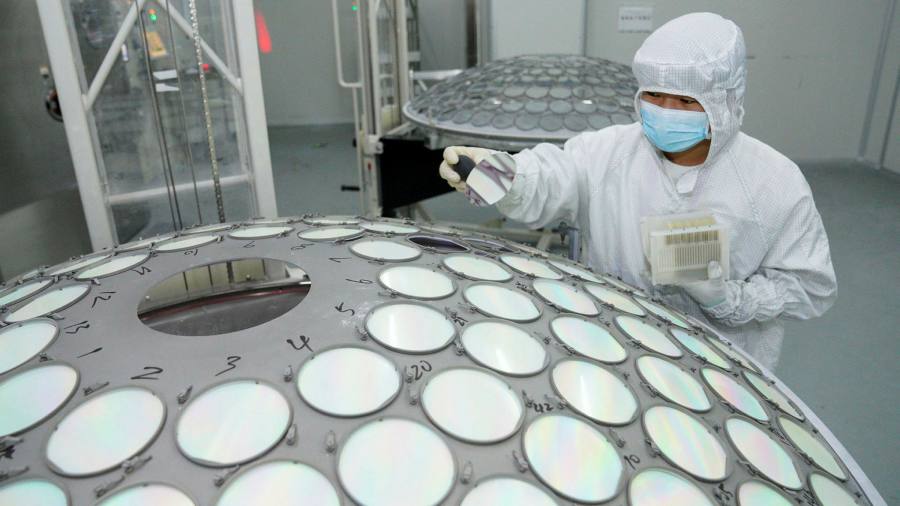

Taiwan Semiconductor Manufacturing Company, the world’s largest contract chipmaker, is preparing to spend another $44bn on expanding capacity this year. Likewise, Intel is planning a multiyear expansion worth up to $100bn building what could become the largest fab ever.

Such splurges in the past have led to overcapacity, often coming as demand softens. And now warnings are starting to appear about current conditions. Several analysts say the pronounced chip shortage that has kept fabs full and driven prices up could turn into a glut as early as 2023.

“There is the concern that there is going to be overcapacity,” said Dylan Patel, a chip expert at SemiAnalysis, a research group. “I do see this cycle being longer than in the past, but I also see the next down-cycle being deeper.”

There have been signs of softening demand in some segments for months now: sales of Chromebooks dropped sharply after the pandemic-induced demand for the low-cost laptops for online school lessons was met.

Demand for internet equipment is also slowing as families working from home have upgraded their WiFi gear. Similarly, the growth in sales of LCD television sets and online gaming gadgets is expected to decrease as the easing of coronavirus restrictions allows consumers in Europe and America to go out again.

But many industry experts argue that this is only the beginning, not the end, of an extraordinary boom for the global semiconductor market.

“There is nothing normal about this chip cycle,” said Dan Nystedt, vice-president at TriOrient, an Asia-based private investment company. He added that the disruption caused by the US-China trade war and then Covid-19 led many in the industry to misjudge demand and underinvest. “There are bigger trends going on which are likely to drive up demand for much longer,” he said.

The chip industry was in the past powered by one or two key devices such as the personal computer and then the smartphone. The rise of artificial intelligence is now enabling the use of chips in almost everything from cars to factories to home appliances. Then additional computing power is required to store and process the vast amounts of data gathered on the “smart” devices and infrastructure.

As a result, semiconductor content per device is ballooning. Applied Materials, a US chip equipment maker, predicts that one smartphone will contain $275 worth of chips by 2025, up from $100 in 2015. The chip content per car is forecast to increase from $310 to $690 and per datacentre server from $1,620 to $5,600 over the same period.

Apart from this increase in demand for chips, there is also a structural change in the end market. “For the past 20 years, the main end user has been consumers. But now, the industry may return to a situation where corporates and governments are driving demand,” Nystedt said. “While consumers want low-cost products, enterprises and governments expect quality. This might change the pricing structure.”

Chip executives, therefore, believe that comparisons with the industry’s past patterns, which have seen cyclical drops every two to four years on average, fall short. Moreover, as building state of the art fabs gets ever more expensive, the big jumps in capital expenditure from TSMC and its rivals Samsung and Intel do not mean equally large jumps in capacity.

“Most people would be amazed to see that these investments will translate into a 10 to 15 per cent increase of capacity per year over the next few years,” said Sebastian Hou, managing director at Neuberger Berman, the investment manager. “That is probably just enough to meet the increase in demand.”

Add to this dynamic is the weakening of global supply chains as governments from the US and Europe to Japan and China seek to build local capacity to hedge against both geopolitical rivals and risks of disruption like in the pandemic. This means customers are likely to build greater stockpiles of chips to ensure they have enough.

“We were very efficient under the globalised supply chain, but efficiency will decrease,” said Hou. “More capacity will be built than was considered necessary under the globalised supply chain.”