Evergrande’s international bondholders are bracing themselves for a prolonged restructuring process as investors attempt to recoup funds loaned to China’s most indebted property group.

Fitch on Thursday placed the real estate developer into “restrictive default” after Evergrande failed to make a crucial interest payment by the time a 30-day grace period expired. The missed instalment has dashed the hopes of some investors, who were expecting the sprawling company to make a last-minute payment.

“I thought we were going to receive [the interest payment],” said one investor in the group’s bonds who asked to remain anonymous.

Evergrande, with its more than $300bn in total liabilities, has come to embody the broader sector’s debt woes. Chair Hui Ka Yan was summoned by Chinese government officials last Friday after the property developer warned it might not be able to meet its financial obligations. A risk committee was then formed on Monday in which the majority of members were representatives of state-owned enterprises.

International bondholders are now preparing for a restructuring process in which their efforts to recoup value will rely on negotiations with not only the company but also several levels of the Chinese government as the country seeks to limit any fallout from a wider property slowdown.

“Beijing has made it clear that the first priority in the restructurings will be to protect homebuyers,” said Paul Lukaszewski, head of corporate debt for Asia-Pacific at Abrdn. But he added that this priority was “not necessarily against the interests of creditors”.

Evergrande has sought for months to keep its real estate projects running in order to maintain the flow of cash through its business — often with government involvement — which is critical to creditor hopes of a recovery. But it has also sought to raise cash through the sale of assets, raising concerns among debt investors that value remaining in the business could be directed elsewhere.

In October, on a call to bondholders held by law firm Kirkland & Ellis and investment bank Moelis, advisers expressed concerns over Evergrande’s attempts to sell its listed property services company, which ultimately fell through, as well as a stake in a regional bank in China, which was used to repay money it owed to that bank.

Lukaszewski said investors would be “watching very closely as to whether the restructurings are managed to protect the interests of creditors or whether they result in value destruction from the forced sale of assets at steep discounts”.

Another investor who has closely observed the situation but has not invested in Evergrande said “the government is watching where the debt is pricing” and suggested a recovery of 20 to 40 cents on each dollar lent was likely. “Chinese restructurings are like horse-trading. They have to be consensual. You can’t chase directors. You can’t enforce security on shore. You have to play ball with the government,” the person said.

‘The world is watching’

The inclusion of international bondholders in the restructuring process has turned what might otherwise have been a largely domestic phenomenon into one with direct links to the world’s biggest financial centres, from London to New York.

The investor who expected to be paid on Monday noted, aside from any legal avenues available to them, a “reputational component” to the Chinese government regarding whatever happens next. “The world is watching,” he said. “That is a big piece of our leverage”.

International investors have for months closely watched Evergrande’s offshore subsidiaries, such as its property services business and its Hong Kong-listed electric vehicle company, in the belief that they will have recourse to such assets in the event of a failure. The latter has yet to sell a vehicle, and its share price has collapsed by 90 per cent this year after surging at the start of 2021.

Markets and authorities are also focused closely on the treatment of the parties across Evergrande’s vast balance sheet. Yi Gang, governor of the People’s Bank of China, said on Thursday that the rights of investors would be respected. Days earlier, the central bank unleashed almost $200bn of fresh liquidity into the financial system by cutting the reserve requirement ratio, a key rate for banks, in an apparent attempt to ease worries over the embattled company.

One bond investor in mainland China said there were few issues with prioritising homebuyers or migrant workers, but helping investors who lent on the local market at the expense of dollar bondholders would be a “deal breaker”.

“That could prompt global investors to lose faith in China’s offshore high-yield bond in general and no other Chinese developers would be able to access foreign capital going forward,” he said.

Real estate developers like Evergrande have relied heavily on international markets to fund their projects in mainland China, and the firm counts well-known companies like Ashmore and BlackRock among its offshore investors.

The Chinese property sector makes up a large portion of Asia’s entire high-yield bond market, where Evergrande has $19bn of debt outstanding. Kaisa, the second-biggest borrower with $12bn outstanding, was also placed into default by Fitch this week after failing to repay a maturing $400m bond on Tuesday.

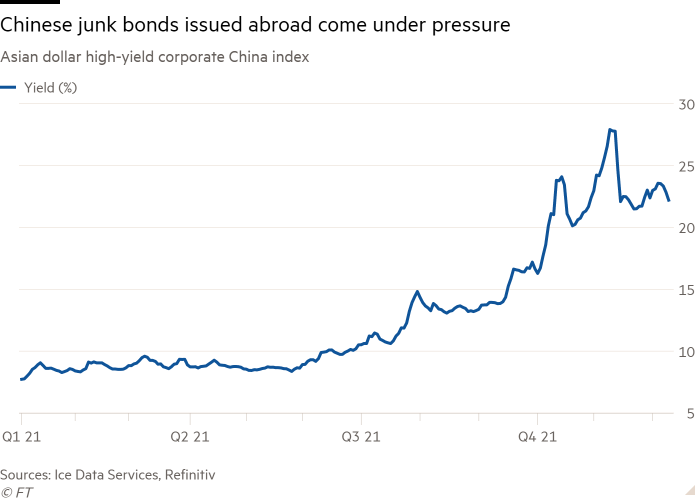

Despite Evergrande’s default arriving this week, the market has improved compared with last month. An Ice Data Services index of riskier Chinese corporate issuers shows average yields at about 23 per cent, compared with close to 30 per cent a month ago but just 14 per cent at the start of September. Markets have also opened to new borrowing from developers after a period in which they were closed, and efforts from the government to restrict the scale of borrowing across the real estate sector have shown signs of easing.

“It seems that we are approaching an inflection point,” said Arthur Lau, co-head of emerging markets fixed income at PineBridge Investments, who suggested the reserve requirement ratio cut by China’s central bank showed the policy “has turned more supportive”.

“I think Beijing realises the potential implication [of a slowdown],” he added.