China’s ride-hailing app Didi will make its debut on the New York Stock Exchange after defeating Uber and becoming dominant on the streets of the country’s major cities, but with worries over growth and regulation on the horizon.

Under the name of its holding company Xiaoju Kuaizhi, Didi aims to raise $3.9bn in one of the largest foreign IPOs since the 2014 Alibaba offering, at a valuation of $64.7bn in the middle of its price range.

The target is similar to the $65bn valuation at which private investors bought into the company in a 2018 fundraising, perhaps reflecting how investor interest in ride-hailing has waned in the wake of a disappointing 2019 IPO for rival Uber.

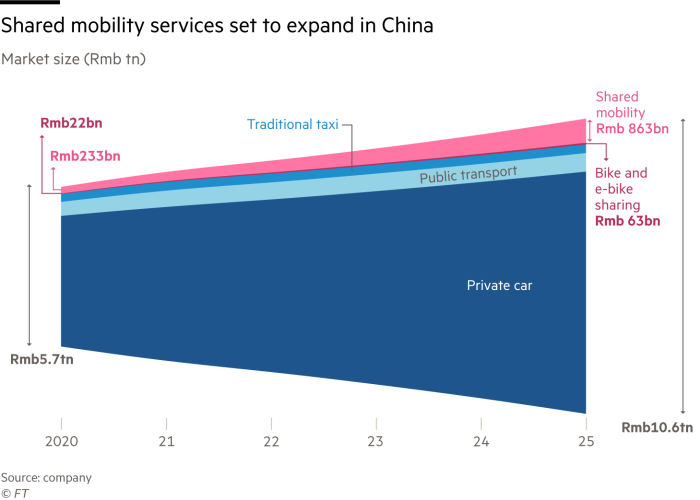

Unlike when Uber came to the market, Didi can boast profitability in its core rides business since 2019, on an adjusted ebitda basis. That core business makes up 94 per cent of Didi’s revenues of Rmb142bn ($22bn) in 2020.

This is a far higher share of revenues than at Uber or Grab, which rely on fast-growing but lossmaking food deliveries for 35 per cent and 49 per cent of revenues respectively. In China, Didi is shut out from the delivery sector by huge rivals Meituan and Ele.me.

But while Didi’s main business is profitable, its margin on each ride that it books is far lower than that of international rivals, at about 3 per cent, compared to 20 per cent for Uber.

Coronavirus lockdowns saw Didi’s bookings fall by a third in the first quarter of last year but China’s strict and largely successful containment of the virus meant its rides business grew year-on-year in the second half of 2020 and only fell 4.8 per cent for the year.

In the first quarter of 2021, Didi achieved an overall positive net income for the first time, largely due to the deconsolidation of its group buying business, Chengxin Technology, that brought in Rmb9.1bn ($1.4bn).

But analysts questioned whether Didi may be reaching saturation in China’s largest cities, such as Beijing and Shanghai, which account for half of its bookings, and whether it can spin up new ventures to boost its growth.

“The main question for Didi is whether its core China mobility can generate enough financial dry powder to fund its emerging new business, such as autonomous driving,” Bernstein analysts wrote in a recent note.

The head of capital markets at one US bank in Hong Kong said that an initial valuation IPO target of $100bn was “never a reasonable starting point” because of the limitations of Didi’s market. “Their big issue is they won’t easily expand outside ride-hailing like Uber did. The equivalent of Uber Eats and logistics are already crowded with deep-pocketed incumbents in China,” the person said.

Overseas, Didi has expanded to large developing economies, such as Brazil, but its non-China business only accounts for under 2 per cent of revenues.

Its dominance in China, however, is unquestioned. Since buying out Uber in 2016, Didi has grown to account for 90 per cent of all online car bookings in 2020, about two-thirds of which come from the top 30 cities.

It does have some competition in smaller cities and towns, with more than 200 rivals operating across the country. T3, a rival backed by Alibaba, Tencent and three Chinese carmakers, has been successful in building market share in Nanjing and Chongqing because of its low prices and self-owned fleet.

“Right now the profit is big, but as competition heats up in smaller cities they will have to bring down prices,” said Cherry Leung, a Bernstein analyst.

But Didi’s backers argued that its profitability is scalable because its competitors are unlikely to engage in a three-way price war fought between Didi, domestic rival Kuaidi Dache and Uber, from which Cheng Wei, Didi’s chair, emerged victorious in 2016.

Cheng and Jean Liu, a former Goldman Sachs banker who became Didi’s president in 2015, have so far avoided having to shell out further expensive subsidies to fend off rivals.

“It’s a very simple question: if you want to do the same as Didi, are you willing to burn $20bn on attracting users?” said Kevin Wang, a founding partner of Ameba Capital and an early investor in Kuaidi Dache, which merged with Didi in 2015.

After conceding defeat to Didi, Uber has retained a sizeable stake, now about 12.8 per cent. Other major investors include SoftBank’s Vision Fund, with 21.5 per cent and Tencent, with 6.8 per cent.

More pressing than competition is the question of whether Didi can navigate tightening regulatory scrutiny during Beijing’s sweeping crackdown on technology groups deemed to have grown too powerful, too quickly.

The company has come under fire for a range of issues from failing to ensure the safety of passengers to concerns of unfair competition and low pay for drivers.

Earlier this month, a financial publication under the official Xinhua news agency said that antitrust investigations were a “hanging sword” over the IPO, citing concerns over price fixing and an investigation into Didi’s deal to take over Uber’s China business, few details of which have ever been released.

In May, Didi executives, alongside more than 30 other ride-hailing companies, were summoned by the Ministry of Transport over concerns about drivers’ pay, after complaints that Didi was taking a 30 per cent cut of some fares.

The company has said that the breakdown only applied to under 3 per cent of cases and vowed to do better to ensure fair pay for drivers.

Even so, the company has been sent a clear warning from authorities: “If Didi does not rectify its behaviour immediately, there could be further escalation of regulatory actions,” said Angela Zhang, a scholar of Chinese antitrust law at the University of Hong Kong.

In the future, Didi still sees promise in autonomous driving, in the hope of cutting out the need to pay drivers, which accounts for 50 per cent of the company’s costs.

But it has taken a more cautious approach than rivals such as Baidu and AutoX, an Alibaba-backed start-up, which have begun removing safety drivers from vehicles. It secured a licence to carry passengers in self-driving cars in Shanghai last year, but has said little about its trials.

Zhang Xiang, a China-based independent automotive analyst, said that Didi’s autonomous driving investment is a way to distinguish itself from Uber after the US company abandoned self-driving in late 2020 and to potentially secure a high valuation for its autonomous business.

“It makes zero sense to launch as a pure autonomous robotaxi service,” said one of Didi’s early investors. “It will have to be hybrid built on Didi’s mobility business, which has had many years to build a back-end tech platform.”

Additional reporting by Emma Zhou in Beijing