Stocks go up, stocks go down, you can’t explain that…

Or maybe you can, if the stock happen to be a biotech that just flunked a clinical trial. Which leads us nicely to Graybug Vision (GRAY). Or not so nicely if you happen to be an investor.

Shares cratered by a dispiriting 51% yesterday after the eye disease drug maker released preliminary data from the Phase 2b ALTISSIMO trial of GB-102 – the company’s twice-yearly intravitreal injection of sunitinib – and candidate for the treatment of wet age-related macular degeneration (wet AMD).

Investors were let down by a different set of data, which showed that the Best-corrected visual acuity (BCVA) of the 1mg GB-102 arm, came in 9 letters below the control arm of Eylea, Regeneron’s competing product.

On the plus side, after participants took 1mg of GB-102, the treatment displayed promising duration data with approximately 48% of patients staying treatment-free for over 6 months. Additionally, 62% of patients did not need any treatment for at least 4 months or more, with an overall median duration of 5 months. GB-102’s safety profile was favorable, too.

Despite being a secondary endpoint in the Phase 2b trial, BCVA is a major primary endpoint for registrational Phase 3 studies in wet AMD, and therefore, a potential key element in the treatment’s overall success.

Given that GB-102 showed very stable BCVA in the previous Phase 1/2 studies, Leerink analyst Marc Goodman considers the result a “negative surprise.”

“Management doesn’t have a good explanation for this result and will need to investigate this unexpected outcome further, but we are not surprised that the stock is off significantly, as investors are also clearly disappointed by the vision results,” Goodman said. “While we look forward to seeing additional granular data from the ALTISSIMO trial before making any changes to the numbers, we are lowering our POS [probability of success] today from 50% to 25%.”

The disappointing data also results in a cut to Goodman’s price target, which is reduced from $45 to $23. Despite the severe haircut, the figure still represents possible upside of a hefty 210%. To this end, Goodman’s rating stays an Outperform (i.e. Buy). (To watch Goodman’s track record, click here)

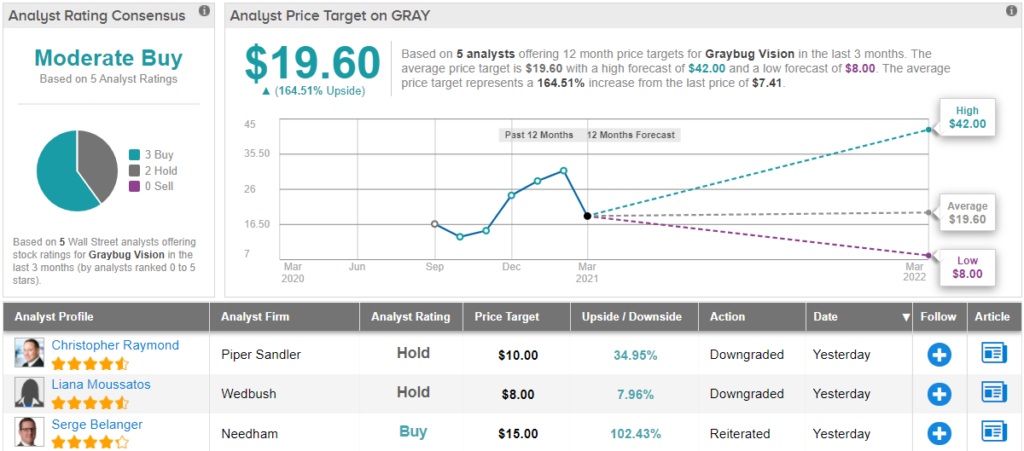

Since the data was published, other Street analysts have been less forgiving, with several downgrading the stock’s rating. Nevertheless, based on 3 Buys and 2 Holds, the stock still boasts a Moderate Buy consensus rating, backed by a bullish $19.60 average price target. Gains of ~165% could be in the cards, should the target be met over the next 12 months. (See GRAY stock analysis on TipRanks)

To find good ideas for healthcare stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.