Banks are in no rush to bring their employees back to the office.

Last month, as novel coronavirus infection rates surged nationwide, JPMorgan Chase, Wells Fargo, U.S. Bancorp and M&T Bank once again delayed their target dates for large-scale office reopenings. Fifth Third Bancorp, which started to bring thousands of employees back in mid-October, halted those plans just two weeks later, citing an increase in COVID-19 cases across its 10-state footprint and subsequent school and business closures due to lockdowns.

The latest timeline revision reinforces the unpredictable nature of the health crisis, which has forced hundreds of thousands of nonbranch bank employees to work from home since March.

Those banks that looked to the fall for a return date are now kicking out decisions until at least next spring, said Pieter van den Berg, managing director and partner at Boston Consulting Group, who leads the firm’s corporate banking segment in North America.

“First banks were planning for the fall, then for January and now that is getting pushed back again,” van den Berg said. “And while the system is working well, probably much better than expected, there is a sense that the uncertainty is weighing on people and employee morale.”

While banks have largely kept branches functioning — and are trying to keep those offices open during the latest increase in cases — the same is not true of administrative and back-office centers. Like companies nationwide, banks in March took swift action to position their noncustomer-facing workforces to work remotely as a means to slow the spread of the disease

During the early months, more than 85% of Bank of America’s workforce shifted to work-at-home. At Citigroup, nearly 90% went remote, while 75% did the same at Wells Fargo.

JPMorgan was among the first in the industry to call workers back to the office. In September, the largest U.S. bank by assets brought some sales and trading employees back to Wall Street, but days later had to send some of the workers home after a staffer tested positive for COVID-19.

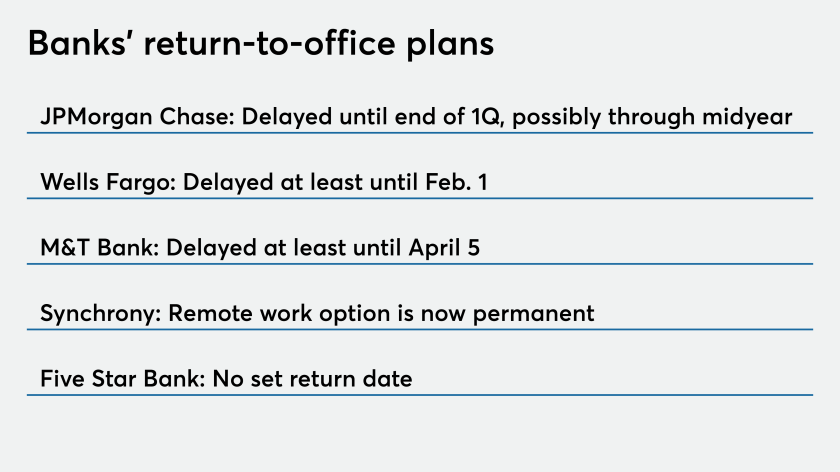

In mid-November, the bank pushed out any sort of mass return of its workforce, telling employees in a memo that the current remote work setup will be in place “until the end of the first quarter and possibly through mid-year.” The bank emphasized the ongoing need for flexibility, saying decisions will be based on local circumstances and could vary by business line.

“As part of this flexible approach, we monitor the evolving pandemic landscape daily and have strong safety procedures in place to bring employees back to the office or to pause or reverse our plans when required,” the note said.

Other banks are making similar decisions. San Francisco-based Wells Fargo now says its work-from-home policy will remain in place through at least Feb. 1, 2021. U.S. Bancorp in Minneapolis pushed out any sort of large-scale return until the second quarter at the earliest.

More than 200,000 Wells Fargo employees and 52,000-plus U.S. Bancorp workers are currently working remotely.

M&T Bank in Buffalo, N.Y., also revised its guidance, saying it will stick to its work-from-home posture for the majority of employees through at least April 5, 2021. The bank said the date is a “checkpoint” at which it will reassess the situation and make a decision based on local and state regulations within its Northeast and mid-Atlantic geography.

“The health and safety of our team members remains our top priority,” the bank said in an email.

Capital One Financial in McLean, Va., told employees working at home to expect to continue doing so through the end of March, not the end of 2020 as it had said earlier. It also has said that most call center staffers will permanently work off-site, even after the pandemic is over. Synchrony Financial in Connecticut went one step further, saying all U.S. employees can work from home on a full-time basis from now on.

It seems likely that more banks will follow suit and give more employees the option of working from home indefinitely. Last week, a Bloomberg report said Deutsche Bank in Germany is thinking about letting most employees work from home two days a week on a full-time basis, allowing for greater flexibility for workers and cutting down on the company’s real estate costs.

Boston Consulting’s van den Berg said he expects banks will want to bring as many workers back to the office as possible, in part because of data security challenges that may arise with work-from-home setups. Still, his colleague Deborah Lovich, a managing director and senior partner, said the unexpected shift home is “a huge opportunity” to rethink how work gets done.

“For the first time we have an opportunity to say, ‘Well, what’s the work and what does it require?’ ” Lovich said. “The whole notion of, ‘We need to get back in, we need to get back in’ is a huge step backward. We also need to ask what employees want and need to be productive.”

Discussions about going back to the office are rampant in banking and all industries where workers were sent home in the spring, said Sharon Randaccio, the president and CEO of Performance Management Partners, a talent management and human resource consulting firm in Buffalo.

“We talk about it constantly,” said Randaccio, a former bank executive who also leads a CEO peer advisory group. “I can tell you that when a few of our larger clients said they weren’t going to bring people back until January, we all said, ‘January? Really? How are you going to keep this [work-from-home stance] going until January?’ But now they’re all proving themselves to be correct.”

Some of her clients are now talking about a June return date, assuming a vaccine is available and distributed and workers feel more comfortable coming together again under one roof.

But there are real challenges that go along with keeping employees separated for so long.

“The biggest issue is culture and how you maintain a culture of engagement when people aren’t bumping into each other at the coffee machine,” Randaccio said. “It’s those informal, unplanned collisions that aren’t taking place and some employees, whether it’s bank officers or front-line customer service reps or tellers, they need that interaction.”

Five Star Bank in Warsaw, N.Y., has not yet set a target date for a mass return to the office. At the start of the pandemic, the $5 billion-asset bank shifted about 70% of its 600-person workforce to work-from-home arrangements and backup crisis locations, but kept branch workers and certain key personnel in the office to perform essential duties. Over the summer, as infections dropped throughout much of the bank’s Central and Western New York footprint, it returned about 120 workers to offices, reducing the percentage working at home to 50%.

Now, with COVID-19 cases spiking again, the bank is preparing to send some workers back home. Executives are projecting that the percentage of remote workers rises to 60%.

President and CEO Martin Birmingham said the bank has made no decisions about enacting permanent work-at-home policies post-pandemic and acknowledged that remote working isn’t a “perfect solution” given the distance it creates between employees and clients.

“Inherently, there are many aspects of banking that benefit from person-to-person interaction around the table and trying to understand what the opportunities and challenges are and solving for them,” Birmingham said. “However, there may be functions suited to remaining remote.”

Randaccio said even if banks send most workers back to the office, things will be different.

“I don’t think we will ever return to the way we were, ever,” she said. “I think we’ve learned there are truly some roles that can be performed very well from home, and I think there are many companies looking at savings in real estate and realizing that maybe we don’t need as much brick and mortar as we thought and that giving people flexibility is important.”