With about two weeks to go until the U.S. election, volatility gauges for stocks and bonds are on different paths. The Cboe Volatility Index — known as the equity market’s “fear gauge” — has been relatively subdued this month in contrast to the ICE BofA MOVE Index, the Treasury market’s equivalent measure.

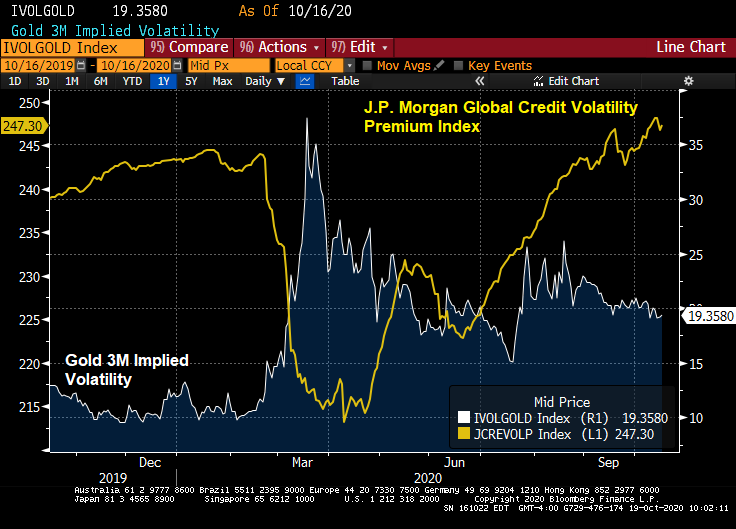

JP Morgan’s Global Credit Volatility premium index has soared since June while gold’s 3m implied volatility is calm.

The Quadratic Interest Rate Volatility and Inflation Hedge ETF has leveled-out after rising from the Covid outbreak.

The US Dollar Swap forward rate has crashed with Covid and has laid flat ever since.

(A vanilla interest rate swap is an agreement between two counterparties to exchange cashflows (fixed vs floating) in the same currency. This agreement is often used by counterparties to change their fixed cashflows to floating or vice versa. The payments are made during the life of the swap in the frequency that is pre-established by the counterparties.)