As the summer reinvestment season heats up, buyers will see a large slate of new sales in the upcoming week, led by issuers in New York, Texas, Maryland and Virginia, which are dominated by taxable offerings.

There will be nearly $14 billion of new issues in the height of the summer as issuers clamour for low rates and investors stomach those low rates.

It’s a very uncertain time for state and local government issuers, but the bottom line, sources said, is they are going to take advantage to the record-low rates and sell as much debt as they can during this time.

Municipals finished stronger on Friday, with yields on the AAA scales falling as much as four basis points.

The forces of supply and demand continued to battle each other during the week as the market couldn’t get enough of the available supply — a trend that should persist, many municipal sources said.

Why taxables? Because, sources said, it makes the most sense for issuers right now, without an exempt refunding option.

“What should concern issuers is that Washington is in disarray. Certain folks know that state and local governments have the option right now to simply sell taxable debt in lieu of exempt refundings. And anything that can sneak through on the federal level won’t be perfect,” a Washington-based source said. “Whether it is a direct-pay option or the return of exempt refundings — it’s pretty much anyone’s guess. But everyone is hopeful that Congress recognizes the needs for state and local governments to function properly, they will need some sort of subsidy.”

Trading was relatively sparse. NYC TFAs, 5s of 2023, traded at 0.24%. Georgia GOs, 5s of 2029 landed at 0.76%-0.75%. Texas waters, 5s of 2032, at 1.09%-1.10%. Dallas waters, 4s of 2039, at 1.59%-1.58%.

Out a little longer, NYC TFAs, 4s of 2045, 2.11% to 2.08%.

Primary market

Market participants expect almost $14 billion of supply to flood into the market in the upcoming week.

The New York State Urban Development Corp.’s $2.3 billion of tax-exempt and taxable general purpose state personal income tax revenue bonds will lead the way.

BofA Securities will price the deal on Thursday.

Morgan Stanley is set to price Texas Transportation Commission’s (Aaa/NR/AAA/AAA) $1.047 billion of taxable general obligation mobility fund refunding bonds on Wednesday.

Citigroup is set to price the Virginia College Building Authority’s (Aa1/AA+/AA+/NR) $703.82 million of revenue bonds on Thursday.

The deal consists of $362.33 million of Series 2020A tax-exempt educational facilities revenue bonds and $341.49 million of Series 2020B taxable educational facilities revenue and revenue refunding bonds for the 21st Century college and equipment programs.

Goldman Sachs is set to price the Rector and Visitors of the University of Virginia’s (Aaa/AAA/AAA/NR) $600 million of taxable general revenue pledge bonds on Tuesday.

JPMorgan Securities is expected to price on Wednesday the Maryland Health and Higher Educational Facilities Authority’s (A2/A/NR/NR) $602 million of taxable revenue bonds for the University of Maryland Medical System.

In the competitive arena, Montgomery County, Md., is selling $852.39 million of general obligation bonds in three offerings on Thursday.

The state of Washington is selling $625.685 million of general obligation bonds in four offerings on Tuesday.

Supply and demand and the ‘cheap’ muni market

Michael Pietronico, chief investment officer at Miller Tabak Asset Management, expects “very solid demand” remaining in place for the foreseeable future as supply continues to be absorbed quite easily.

“Our view is that credit spreads will continue to grind tighter as buyers look to enhance income in a yield-starved world,” he said on Friday.

Transportation is one sector that offers value, according to Pietronico, even as COVID-19 continues.

“Some credits within this sector are trading at spreads that are generously wide, and should a vaccine emerge later in 2020 significant upside exists with these bonds,” Pietronico said.

Munis remain the cheapest U.S. fixed-income asset class, BofA said in a Friday market report.

“Treasury rates went nowhere over the past two weeks, while stock market indexes are approaching their June high. High-grade corporate bonds’ relative richness remains unchanged,” BofA municipal strategist Yingchen Li and Ian Rogow said.

“Likewise, tax-exempt munis’ cheapness to corporates saw no improvement either,” they wrote. “Munis remain the cheapest U.S. fixed-income product.”

They noted that municipal issuance has been strong recently, with a rebound in taxable muni issuance due to the resurgence of taxable advance refundings.

“Despite the pandemic’s market disruption in March to May, year-to-date taxable muni bond issuance totaled $53 billion, on track toward our $105 billion target for the year,” they said. .

However, they noted that green bonds issuance was running ahead of estimates.

“We previously estimated 2020’s green bond issuance between $9.5 billion to $12.9 billion. Bloomberg data shows that $9.0 billion of green bonds issued in 1H20; our estimates may have been too conservative,” they said.

They also pointed out that from January 2015 to June 2020, New York and California issuers sold nearly $26 billion of muni green bonds, accounting for over 55% of the $46.1 billion sold over that period.

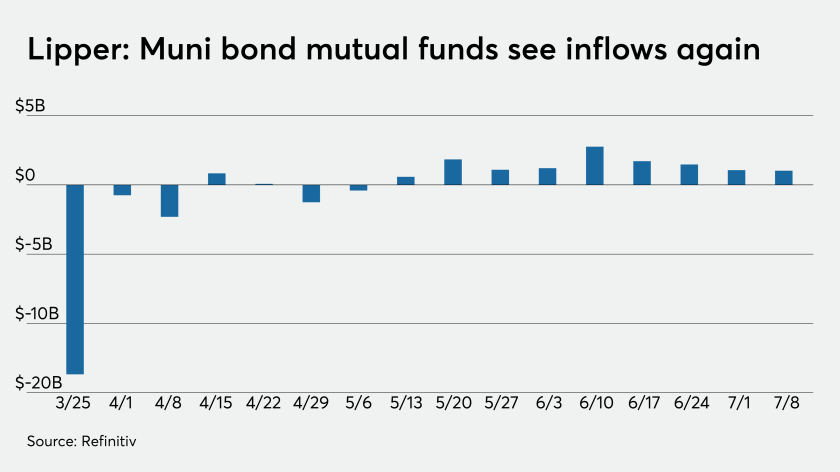

Lipper reports $1B inflow

Investors remained bullish on municipal bonds and continued to put cash into bond funds in the latest reporting week.

In the week ended July 8, weekly reporting tax-exempt mutual funds saw $1.024 billion of inflows, after inflows of $1.065 billion in the previous week, according to data released by Refinitiv Lipper Thursday.

It was the ninth week in a row that investors put cash into the bond funds.

Exchange-traded muni funds reported inflows of $379.709 million, after inflows of $385.850 million in the previous week. Ex-ETFs, muni funds saw inflows of $644.251 million after inflows of $679.370 million in the prior week.

The four-week moving average remained positive at $1.318 billion, after being in the green at $1.752 billion in the previous week.

Long-term muni bond funds had inflows of $617.441 million in the latest week after inflows of $768.699 million in the previous week. Intermediate-term funds had inflows of $73.818 million after outflows of $9.068 million in the prior week.

National funds had inflows of $951.064 million after inflows of $1.044 billion while high-yield muni funds reported inflows of $85.577 million in the latest week, after inflows of $119.298 million the previous week.

Secondary market

Municipals were stronger according to readings on MMD’s AAA benchmark scale Friday. Yields on the 2021 and 2023 maturities dropped three basis points to 0.22% and 0.24%, respectively. The yield on the 10-year GO muni fell four basis points to 0.81% while the 30-year yield dropped four basis points to 1.53%.

The 10-year muni-to-Treasury ratio was calculated at 127.6% while the 30-year muni-to-Treasury ratio stood at 115.2%, according to MMD.

“Munis have a firmer tone today,” ICE Data Services said on Friday. “Yields on the ICE muni yield curve are two to three basis points lower on the day. High-yield bonds are one to two basis points lower.”

The ICE AAA municipal yield curve showed short yields moving lower, down two basis points in 2021 to 0.190% and by two basis points in 2022 to 0.208%. The 10-year maturity dropped three basis points to 0.789% and the 30-year fell three basis points to 1.562%.

ICE reported the 10-year muni-to-Treasury ratio stood at 134% while the 30-year ratio was at 116%.

The IHS Markit municipal analytics AAA curve showed the 2021 maturity yielding 0.21% and the 2022 maturity at 0.24% while the 10-year muni was at 0.84% and the 30-year stood at 1.57%.

BVAL reported one basis point drops on the one-year at 0.18%, two-year at 0.23%, 10-year down three basis points to 0.79%, while the 30-year was lower by three basis points to 1.57%.

Munis were little changed on the MBIS benchmark and AAA scales.

Treasuries were weaker as stock prices traded up.

The three-month Treasury note was yielding 0.137%, the 10-year Treasury was yielding 0.632% and the 30-year Treasury was yielding 1.324%.

The Dow rose 1.10%, the S&P 500 increased 0.70% and the Nasdaq gained 0.30%.

Lynne Funk contributed to this report.