We are nearing that mid-point in July when I said we would start to see the news turn from euphoria-inducing reopening positives to depression-developing realism.

Speaking of stock-market bulls who are stampeding uphill on the euphoria side, I wrote,

Right now the farce is with them — reopening has arrived! And these stupid people will believe that means they were right about the “V,” virtually assuring they continue to bet the market up for a little while…. The reopening means economic statistics will improve rapidly. That will give a lot of stupid people many reasons to believe they were right to think the obliterated economy would experience a V-shaped recovery.

What they won’t see because they don’t want to see it is that the steep recovery is not going to take the economy back to where it was…. It may take stocks back to their last highs (and beyond!) but not the economy.

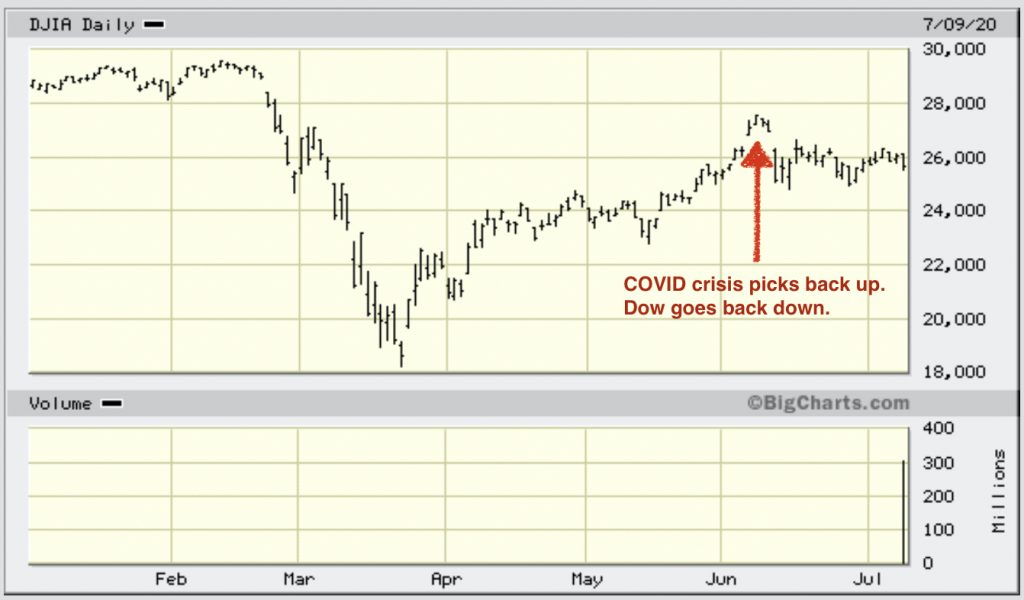

And, so it has tuned out. The Dow and S&P have stalled at about a 60% retracement of their earlier crash, which is right where I said I thought they would. They stopped rising well below their all-time peaks because the COVIDcrisis raised its ugly head (the one caveat I gave for stocks continuing rise to the moon) very quickly after our nationwide economic reopening …

… but massive bets have poured into tech stocks — long seen as the surest bet in a risky marketplace — and have pushed the tech-heavy Nasdaq on a reach well beyond its former peak:

So, we see the stock market proving both claims true — that a rise of COVID-19 would knock the wind out of the euphoric bulls but that, absent a host of new COVID-19 headlines, the bulls would continue to focus on the great reopening news because the worst news would come later.

That is how I read what is happening in this split: money effectively shifted from the more value-driven Dow and S&P where the rise had been going strong into the high-velocity, high-tech NASDAQ to complete the charge up past former highs as I said the bulls would try to do.

The path became narrower; but the tech charge, where most of the testosterone is, continued to drive up the center, pumped by the V-shaped fantasy — pumped so hard that those remaining bulls are paying no attention to the new COVID headlines, while others have fallen to the sides.

“Here’s the full truth,” I said in early June about the euphoria-inducing reopening:

Reopening means, OF COURSE, businesses will start to show rapid improvement, and millions of jobs will certainly come back almost overnight. That’s half the truth. The other half, which investors … won’t see because they don’t want to, is that many businesses will not reopen, and many jobs will not come back…. But guess which half of the truth you get to see first? We’ll be deep into July before we start to see where the rapid recovery stalls out, and then it may take a little longer before investors start to see it because they don’t want to.

Yet, that truth is already flooding in for those who are willing to see it, and I’m going to lay out the broad overview of it here and then give a whole deluge of short facts tomorrow:

Now it really is a retail and restaurant apocalypse

While I said retail — because it was already dying — would show the worst damage, I also noted in other articles that restaurants would suffer similarly broad and quick deaths because they are typically run on thin margins.

So, here is where we are on reopening for those segments of the economy that I said would become the first devastating news to materialize, particularly restaurants, retail and unemployment. The latter I said would hold at deep recession levels. Now that reopening appears to have gone about as far as it is going to go because some states have reversed it, while others are going no further on an indefinite basis, we are already at the point where reopening is climaxing.

First, here’s a real ground-level (Main Street) view of how jaw-dropping the destruction to restaurants turned out to be (worse at this early date than even I thought it would be):

53% of restaurants closed amid coronavirus have shuttered permanently, Yelp data shows.

In March, restaurants had the highest numbers of business closures listed on the app compared to other industries, and the rate of closure has remained high. Of the businesses that closed, 17% are restaurants, and 53% of those restaurant closures are indicated as permanent on Yelp….

During the peak of the pandemic, the number of diners seated across Yelp Reservations and Waitlist dropped essentially to zero. In early June, numbers of diners seated are down 57% of pre-pandemic levels.

The National Association of Restaurants had estimated 15% of restaurants would close for good. I had noted another publication, Open Table, that estimated 25% would never reopen. I ventured 20% would not reopen but then many others that did reopen would close under the partial-opening restrictions in most states, so that we’d eventually be down about 40%.

It looks like many of the latter kind (the ones that would reopen and then give up) were smart enough no to even give partial-reopening a try because, as I said, most restaurants will run at a loss throughout the period of partial reopening. They cannot make it with their customer base cut in half … or worse.

53% of those listed on Yelp (which is most) that closed are gone for good. That is absolutely catastrophic. That’s the number on Yelp that have so fully given up that they have already reported to their customers they will never reopen!

If you’ve been thinking I have been too bearish about. all of this, wait until you see how bad it may become once many of those that have reopened give up the ghost in exhaustion:

85% of independent restaurants may go out of business by the end of 2020, according to the Independent Restaurant Coalition…. Independent restaurants, which comprise 70% of all restaurants, rely more heavily on dine-in revenue than chains and don’t have a corporate safety net or support system to fall back on.

As for the retail apocalypse that I’ve been describing for, at least, three years,

41% of businesses closed on Yelp have shut down for good during the coronavirus pandemic. Retail was hit the worst…. Los Angeles recorded the largest total number of closures with 11,774 business establishments shuttering, but Las Vegas has had the highest number of closures relative to the number of businesses in the city at 1,921…. Shopping and retail stores have suffered 27,663 closures.

We are not even to the middle of July, and already the first wave of permanent damage to wash over us is massive. Almost beyond belief! It’s a total tsunami of “permanent” business destruction, and a lot more waves are coming from all the businesses that are impacted by the businesses that have just shut down for good!

Yet, do you think I could convince bullish investors on other sites that we are going beyond a recession and into a second Great Depression and that the stock market is raving mad? Not even with my best arguments.

However that, too, fits exactly what I predicted, which was that bull-headed stock traders would certainly be the last to figure this out. I was so certain the lunacy and complete denial would keep charging ahead that I said I was going to bet my own retirement money on it in stocks for a short ride up, unless and until the COVIDcrisis came crashing back into the party with new headlines of rising cases and deaths. It almost immediately did, making the ride shorter than I anticipated because that was my self-imposed stop for getting out of the risk.

I wanted to put my money where my mouth is to prove how much I believed what I was saying, and I would have made money had I stayed in because most of the stock funds I invested our three small 401Ks in were heavy in tech. However, I adhered to my stop when COVID crashed the party with rapidly rising cases.

So, it was a dumb bet in terms of hoping the health crisis would stay down for the first couple weeks of reopening; but it was not at all wrong about how far the market euphoria would keep pushing even past the start of truly depressing news that is now coming in before the mid-July date I gave for the reversal in the economic news flow. Today’s rise in the Nasdaq in the face of today’s terrible economic news, shown below, affirms that.

Epic Great-Depression-level unemployment begins new epoch in US history

I noted in my article referenced above that the biggest upward driver for the stock market’s irrational exuberance would be the certain-to-be-seen rapid turnaround in job losses from the worst losses in history to the best gains in history. That certainly has turned out to be the centerpiece of the narrative the market is riding on; but the deeper truth, I said, would be…

Unemployment will remain high enough to still be considered typical of a recession because marginal businesses did not reopen (including particularly retail stores that were barely holding on)….

And, so, here is how all of that is coming together in this morning’s hot news:

As the number of new coronavirus cases in the United States rose to a single-day record [Wednesday], fresh government data on Thursday showed another 1.3 million Americans filed for jobless benefits, highlighting the pandemic’s devastating impact on the economy. More than 60,000 new COVID-19 infections were reported on Wednesday and U.S. deaths rose by more than 900 for the second straight day, the highest since early June…. The grim U.S. numbers come on top of extraordinarily high jobless figures, although they came in lower than economists had forecast…. Initial unemployment claims hit a historic peak of nearly 6.9 million in late March. Although they have gradually fallen, claims remain roughly double their highest point during the 2007-09 Great Recession. With coronavirus cases rising in 41 of the 50 U.S. states over the past two weeks, according to a Reuters analysis, many states have had to halt and roll back plans to reopen businesses and lift restrictions.

Reuters lead competitor carried a similar kind of report a few days ago:

US unemployment falls to 11%, but new shutdowns are underway.

U.S. unemployment fell to 11.1% in June as the economy added a solid 4.8 million jobs, the government reported Thursday. But the job-market recovery may already be faltering because of a new round of closings and layoffs triggered by a resurgence of the coronavirus…. While the jobless rate was down from 13.3% in May, it is still at a Depression-era level. And the data was gathered during the second week of June, just before a number of states began to reverse or suspend the reopenings.

That’s how bad it it … just in the broad sweep! And that was measured before states started to reverse their reopening plans. That unemployment was, in other words, solely due to the effects of the initial shutdown continuing to play through.

An epic conclusion

These numbers are truly as grand on a historic scale as I said the next recession would be when I named what was coming “The Epocalypse” a few years ago. In fact, the data are worse by far than what I thought the starting data for permanent destruction would be back when I started (a couple of months ago) to lay out the timeline for how all of this would go down.

While the pandemic response is clearly a huge factor in the present crisis, the economy is collapsing much harder than it would have with deeper, more permanent destruction than our politicians ever thought their closures could cause because the economy was a house of cards ready to collapse in the first place.

They didn’t see what destruction their actions would wreck upon the economy because they were blind to how fractured our economy was by the deep flaws I’ve been pointing out for years. Our social structures are caving in at the same time, as I also said would be part of The Epocalypse.

Shortly after the COVID-crisis had taken down the stock market in a Great-Depression-era sized crash, I started making it clear that the worst numbers — the permanent damage — wouldn’t even start to become known until mid-July. Now I can say that train of facts has started pulling into the station a week early.

This article presents the broad picture of just how much this recession is following the exact fast track I said it would … including the stupid stock market. Tomorrow, I’m going to lay out a finer-grained picture by presenting numerous headlines as thumbnail prints of the economic collapse that is gaping now open beneath us.

This is not just a recession. It may even become worse than the Great Depression. If these numbers hold for permanent business closures (and there is no reason to think they won’t) and new unemployment claims continue as they are now starting to crystalize even before the middle of July, this will certainly develop into the complete economic and social collapse I call “The Epocalypse.”

Death of the dollar, death of money as we know it.

As I wrote in my latest Patron Post, this collapse may also now include a global dollar collapse, which will change the world and the United States’ relationship to it. In addition to all I wrote in that article on the possibility of a dollar collapse and its effects, which was quite extensive, I am now including here in this article an interview with Shadowstats’ John Williams on that same subject.

Williams has been an economist since the Nixon administration more than forty years ago. He is the one I sometimes go to for quotes on real economic data without all corrupt revisions the government has worked into its formulae since the dollar lost its last hold on gold in the Nixon era and the government had to start compensating for the truth.

Williams validates everything I wrote this week about a possible dollar collapse (and that means the Fed’s destruction along with it), saying the dollar is looking seriously imperiled this year.

As I stated at the start of my Patron Post, I’ve never written about the collapse of the dollar as a possibility in any year until now. I’m not predicting it will collapse this year because I point out in my own article that there are also strong disinflationary forces at work; but this is the first year in which I think it actually could. It is time to be vigilant about it, watching what is happening in foreign currency exchanges and keeping a close eye on what is happening with US inflation (not as falsely reported by the government, but as such stats used to be calculated in the 1970s and still are by John Williams on Shadowstats.com.

I’m putting Williams’ interview in this article, rather than my Patron Post on the subject, because he also spells out why this current economic crisis is going to turn into something even worse than the Great Depression — an all-out “economic collapse.” Like me, he says the roots for all of this were laid in before COVID-19 came along.

Williams also says the recession started last year … when I said it would, though I also said it wouldn’t be recognized until this year:

[embedded content]

If you want more on the possible dollar collapse that may become part of this global catastrophe, it’s in my last Patron Post. But I wanted everyone to have, at least, the gist of what is coming to the world free here on this site through articles like this one that are available to all because of those patrons who generously try to make all of this worth my time. (It remains mostly a labor of love and earnest concern.)

You can see that post and everything I’ve written over the past year about the move to central bank digital currencies, the death of cash, and the Fed’s final solutions to its failing recovery as my thank-you to those who go the extra mile and become patrons at the $5 level or above via the link below: