The deferral period ends once guaranteed lifetime distributions commence. We have entered the distribution period. Guaranteed income will be set using an age-based guaranteed withdrawal or payout percentage rate applied to the value of the benefit base. The guaranteed withdrawal rate multiplied by the benefit base sets a guaranteed distribution amount supported for life, even if the contract value of the underlying assets is depleted. Guaranteed distributions may even increase through step-ups if new high watermarks are reached for the underlying asset base on the designated dates when this is checked.

What are the guaranteed withdrawal rates?

For deferred variable annuities with income riders supporting a guaranteed lifetime withdrawal benefit, the guaranteed withdrawal rates or payout rates are most typically based on the age that lifetime guaranteed distributions begin, and on whether the distribution is taken by a single individual or by a couple. These payout rates can vary between companies and even for different versions of variable annuities offered by the same company. The rates are set at the time of the contract and would not change for that contract holder, though over time the rates may change for new purchases.

Getty

For a simple example, a company might offer the following payout rates to single individuals based on the age that lifetime withdrawals begin: 4.5 percent for ages fifty-nine to sixty-four, 5 percent for ages sixty-five to sixty-nine, 5.5 percent for ages seventy to seventy-nine, and 6.5 percent for ages eighty and over. For couples, payout rates would generally be 0.5 percent less (so, 4.5 percent at sixty-five, for instance) and would be based on the age of the younger person. For couples, another possibility could be that the payout rates remain the same as for singles, but that a higher fee is charged to support the guarantee over the longer expected joint lifetime. Variable annuity payouts generally do not make a distinction between genders, which would provide benefit to longer living women relative to men.

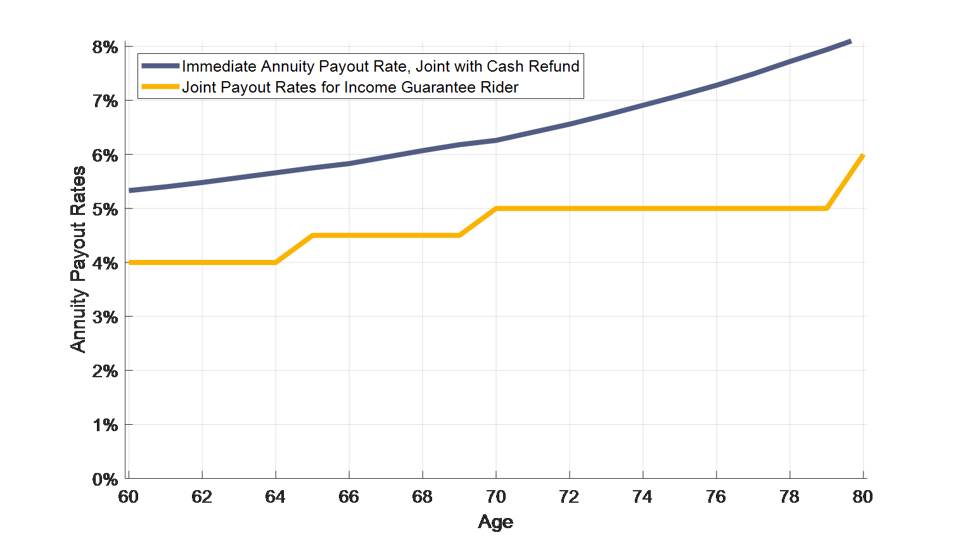

The payout rates on variable annuities at different ages will generally be less than the payout rate offered by an immediate annuity purchased at the same age (although this is not always true, as it may occasionally be possible to find variable annuities with larger income guarantees than an immediate annuity). This can be expected since the variable annuity continues to provide liquidity for the underlying assets and the potential for upside growth in the guaranteed income. However, the question remains about how much less the payout rate is for a variable annuity relative to an income annuity.

Exhibit 5.3 provides an example, showing the payout rates on immediate annuities for couples at different ages alongside the payout rates on the hypothetical variable annuity just described. The immediate annuity payout rates were collected from ImmediateAnnuities.com on January 15, 2019, and they include a cash refund provision to match closer with the death benefit provisions of the variable annuity. The gaps in provided income can be quite large. Payouts are closest after the variable annuity payout increase at age seventy when the immediate annuity provides 25 percent more income, and they are the farthest apart at age seventy-nine when the immediate annuity offers 58 percent more income. We will return to this issue later when we delve into how to think about the upside potential of a variable annuity.

Exhibit 5.3 Guaranteed Withdrawal Rates for Couples Immediate Annuity Payout Rates for Joint and 100 Percent Survivors Benefit with Cash Refund Provision vs. Guaranteed Lifetime Withdrawal Benefit Rate on Hypothetical Deferred Variable Annuity for a Couple

Retirement Researcher

Click here and subscribe to the Retirement Researcher weekly newsletter and receive additional articles, resources, and exclusive invitations to upcoming webinars!

This is an excerpt from Wade Pfau’s book, Safety-First Retirement

Planning: An Integrated Approach for a Worry-Free Retirement. (The Retirement

Researcher’s Guide Series), available now on Amazon