While tax-exempt yields rose slightly Monday, some investors questioned the market’s reaction to ongoing national crises and the associated impact on state and local government finances.

The short end of the curve sold off by three basis points, per triple-A benchmarks.

Part of that had to do with the rally that occurred during May that was most likely overdone. However, what’s occurring in the U.S. public finance markets has been generally muted.

“In the backdrop a plethora of headlines to read through and make sense of is consuming traders, investors and main street folks alike. Protests for racial justice sparked by the recent death of George Floyd at the hands of a Minneapolis police officer (since arrested for murder) has heightened the fear of COVID spreading as thousands march in the streets in over 17 cities nationwide,” said MMD’s senior analyst Peter Franks. “Businesses that were reopening are now shutting their doors as looting and rioting has broken out in many cities. Just when there seemed to be a light at the end of a deep dark tunnel, the country hit a bend in the road and that light seems to be further away now.”

Some investors have reservations the market is not reacting appropriately to the depth of what the economic effects of the protests, combined with coronavirus, will have.

“These have economic impacts on our day-to-day lives and how we interact with each other and that is something that any investor should take a point to consider,” said a New York strategist. “We don’t know how this will play out and if you can’t trade on these types of insecurities I don’t know what you can trade on. It should make us wary of what is coming ahead.”

Looking back, there is a pre- and post-theme to the market.

“March’s dislocation looks somewhat like a bell curve with January, February, April and May’s yields on either side, except that the peak in yields is far removed from a normal distribution,” said Kim Olsan, senior vice president at FHN Financial.

She noted the 5- and 10-year AAA spots have returned to or are through late February’s range following yields that hit 2.50% and higher. And, on the longer end of the curve yields are about 25 basis points off their 2020 lows and well away from 3.50% and higher rates.

“What May’s rally did was to solidify that 1) GO and essential service bonds will remain preferred credits for most traditional inquiry and 2) more impacted sectors like Healthcare and Transportation have found working spread ranges where both new issue and secondary order flow is occurring.”

After posting losses of 2%-3% in April, transportation and healthcare have been able to recover and move closer to flat for the year.

“As the new month begins, the market is precariously balancing heavy (implied) demand against what are growing realities of local and state revenue pressures, all the while trading at ultra-low yields,” Olsan said.

Estimated redemptions of over $40 billion this month should give the reinvestment side of the equation more weight, but there are likely to be occasional pullbacks and distraction later in the month from tax payments coming on July 15th.

Primary market

Action kicked off early as the week’s biggest exempt issuer came to market with a deal offered up to retail investors.

Siebert Williams Shank priced the New York City Municipal Water Finance Authority’s (Aa/AA+/AA+/NR) $630.275 million of Fiscal 2020 tax-exempt water and sewer system second general resolution revenue bonds for retail ahead on the institutional pricing on Tuesday.

The $280.275 million of Series FF bonds were priced for retail to yield 0.52% with 4% and 5% coupons in a split 2025 maturity; 0.79% with a 5% coupon in 2027; 0.88% with a 5% coupon in 2028; 1.76% with a 5% coupon, 1.98% with a 4% coupon and 2.23% with a 3% coupon in a triple-split 2041 maturity.

The $300 million of Series GG-1 bonds were priced for retail to yield 1.08% with a 5% coupon in 2030, 1.94% with a 5% coupon in 2048 and 2.18% with a 4% coupon and 2.45% with a 3% coupon in a split 2050 maturity.

The $50 million of Series GG-2 bonds were priced with 5% coupons to yield 0.50% in 2026 and 0.85% in 2029.

Proceeds will be used to fund capital projects and refund outstanding bonds for savings.

Since 2020, the MWFA has sold over $25 billion of bonds, with the most issuance occurring in 2010 when it offered $3.8 billion of securities.

Secondary market

Municipals ended little changed Monday as geo-political events put a damper on optimism seen from economic data and raised red flags about the future.

Refinitiv Municipal Market Data senior analyst Greg Saulnier said muni trading was quiet in early going as “financial markets grappled with a number of national and global storylines: U.S.-China tensions, growing protests throughout the U.S. over police brutality and racial inequality, coronavirus vaccine developments and economic reopenings all over the world.”

Later in the day, the rally on the short end came to a close as yields move up as much as five basis points. Long yields were little changed.

Trades showed Hamilton County, Tennessee GOs 5s of 2022 at 0.20%.

Georgia GOs 5s of 2023 were at 0.23%.

Maryland GOs 5s of 2023 were at 0.20%.

Out long, New York City TFAs, 4s of 2040, traded at 2.17%-2.16%. Their original yield was 2.56%.

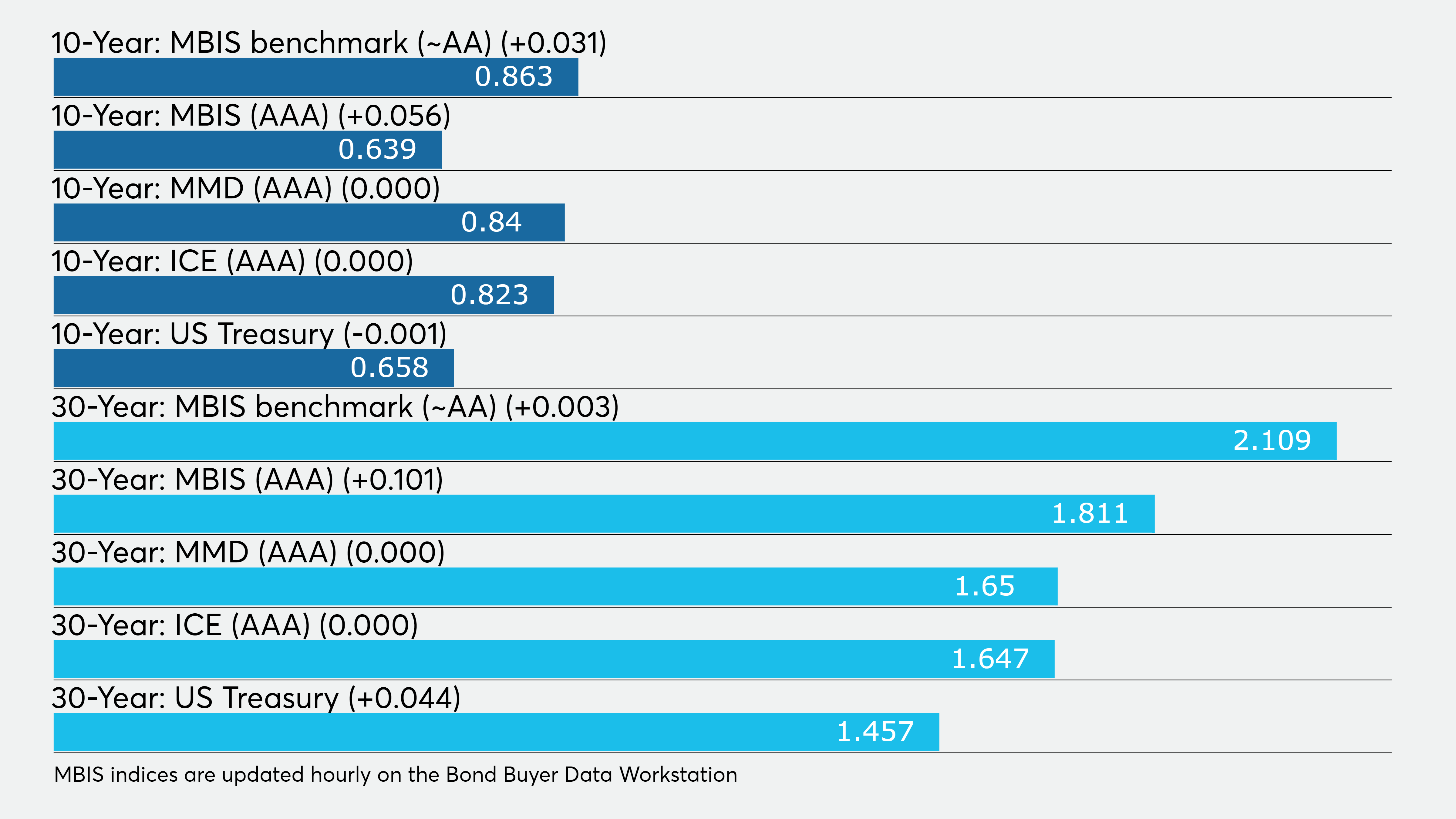

On MMD’s AAA benchmark scale, the yield on the 2021 maturity rose five basis points to 0.16% and increased three basis points in the 2022 maturity to 0.19% while the 2023 maturity was unchanged at 0.23%. The yield on the 10-year GO was steady at 0.84% while the 30-year was flat at 1.65%.

The 10-year muni-to-Treasury ratio was calculated at 126.5% while the 30-year muni-to-Treasury ratio stood at 113.2%, according to MMD.

The ICE AAA municipal yield curve showed yields rising two basis points in the 2021 and 2022 maturities to 0.150% and 0.181%, respectively, while the 2023 maturity was steady at 0.229%. Out longer, the yields on the 10- and 30-year maturities were unchanged at 0.823% and 1.647, respectively%.

ICE said the 10-year muni-to-Treasury ratio stood at 133% while the 30-year ratio was at 111%.

IHS Markit’s municipal analytics AAA curve showed the 2021 maturity at 0.15%, the 2022 maturity at 0.20% and the 2023 maturity at 0.23% while the 10-year muni was at 0.84% and the 30-year stood at 1.64%.

The BVAL curve showed the 2021 maturity rise three basis points to 0.9% and the 2022 at 0.14% up two. BVAL had the 10- and 30-year unchanged at 0.80% and 1.68%, respectively.

Munis were little changed on the MBIS benchmark scale.

Treasuries were mixed as equities were slightly higher in late trading.

The three-month Treasury was yielding 0.138%, 10-year Treasury was yielding 0.658% and the 30-year was yielding 1.457%.

The Dow rose 0.47%, the S&P 500 increased 0.55% and the Nasdaq gained 0.76%.