Investments in 529 plans had hit an all-time high at the end of 2019 — right before the coronavirus pandemic swept through the U.S.

Since then, asset levels have dropped amid market turbulence, and as economic conditions worsen, parents may not be quick to start upping their investments in the plans, according to two new reports.

College savings plans suffered losses ranging from about 5% to 19% in age-based portfolios during the first quarter, according to a Morningstar report, which said “they were also more susceptible to declines than one might expect.”

Based on historical returns, “it would take … roughly a year for a 17- or 18-year-old to recoup the loss,” says Madeline Hume, a Morningstar analyst and co-author of the report.

Meanwhile, some parents are no longer making contributions, and in some cases have withdrawn or plan to withdraw college savings, according to research from Wells Fargo Advisors.

Susceptible to market swings

Before the coronavirus pandemic, assets in 529 plans had surged to $328 billion at the end of 2019, up from $286 billion a year prior, according to Morningstar. But by the end of March, assets fell to $293 billion.

529 plans typically include age-based options, where asset-allocation shifts from stocks to bonds over a 18-year period as a beneficiary nears college enrollment. These portfolio groups are well-diversified and “mostly hold safe, low-yielding fixed-income securities at the end of the glide path,” according to Morningstar.

Amid coronavirus volatility, only age-based portfolios with beneficiaries already enrolled in college performed better than their underlying stock exposure. All the other options captured 100% or more of the downside.

Hume says that fees, riskier fixed income exposure and the poor performance of underlying funds may have contributed to this.

“A little bit of a mixed bag there, but for the portfolios where it really counts — the ones that are approaching college — they held up about as expected,” she says.

Beneficiaries at or near age 18 will need a 3.5% return to recover losses from the past few months, which is “not an unrealistic goal to achieve in less than a year,” according to Morningstar.

Still, there are other considerations at play.

“Families are starting to witness layoffs and children are starting to consider whether they should delay college, or maybe not attend college altogether,” Hume says.

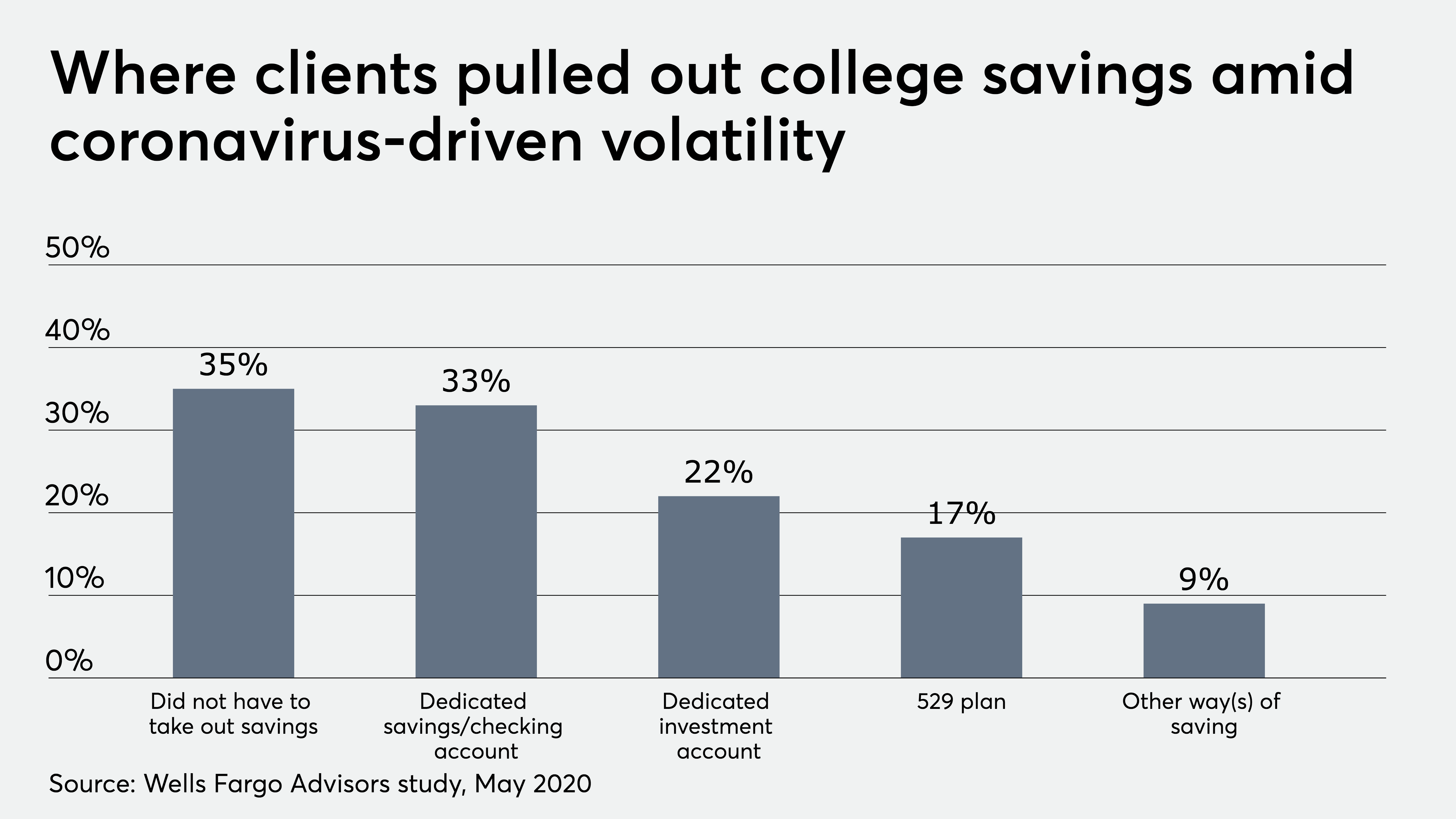

While some clients are no longer able to contribute, others are considering withdrawing funds, according to Wells Fargo Advisors’ research. Forty-two percent of those surveyed said that they are very or somewhat likely to have to take funds out of their college savings in the next six months. Sixty-five percent said they already had.

Under the CARES Act, clients can withdraw money from their 401(k) for coronavirus-related expenses without having to pay the standard early withdrawal penalty. That isn’t the case for 529 plans.

“The earnings portion of that distribution is still going to be subject to ordinary income tax, and potentially a 10% penalty unless an exception applies,” says Tracy Green, a planning and life events specialist at Wells Fargo Advisors.

Clients may want to heed the cost of pulling out funds or skipping contributions with regard to compounding investment returns.

“Even one additional year of contributions can increase the median ending account balance by up to $5,900,” Hume says. “[Clients] also can take tax benefits for contributing to that additional year depending on the state that they live in, whether they have state income tax benefits.”

To be sure, many clients are still contributing to 529 plans. Others may be in a position to use stimulus checks to open up an account for the first time or make a one-time contribution. Grandparents have been reaching out, asking about gifting limits, according to Green.

“Believe it or not, they’re still wanting to put [money] in there,” she says.