“Insiders” recently got a bad rap, as the Feds levied charges on Senator Richard Burr for illegally using information from a closed Senate hearing to avoid a loss in his stock transactions. It was a classic abuse situation, and one that Federal securities regulators work hard to prevent.

But there are always people “in the know,” and it’s only human nature for them to use their knowledge in their trades. These insiders are corporate officers and board members, and they’re charged with running their companies profitably for the benefit of shareholders. It’s accepted that they’ll use their info in their trading, as they almost always own considerable blocks of shares – to keep the playing field level, these insiders are required to publish their transactions every quarter.

And the trading public can use those disclosures to plot an investing strategy. Using the TipRanks Hot Insiders’ Stocks tool, you can see which equities are the target of insider moves, whether those moves are buys or sells, and whether they are informative or simply adjustments to a holding. We’ve pulled up three stocks that have shown recent ‘Informative Buys’ from their corporate insiders. Here are the details.

FlexShopper, Inc. (FPAY)

We will start with an interesting stock. FlexShopper is an e-commerce company, with subsidiaries that operate a lease-to-own online marketplace. Products available include electronics, video games, furniture and home appliances, musical instruments, and health and fitness gear.

The company reported at 8.8% gain in net revenue in Q1. Where most companies took a hit due to the coronavirus crisis, e-commerce was one of the few sectors that saw continued opportunities.

Despite the strong quarterly performance, FPAY shares are down 33% year-to-date. In fact, the share price has slipped down to penny-stock territory, a niche that offers both low prices and high upside potential for investors willing to take on some risk.

The insiders at FlexShopper are clearly willing to do just that. For the last three months, no fewer than four company officers have been making informative buys of FPAY stock. The largest purchaser, Howard Dvorkin, a board member of the company, spent $954,000 on more than 600,000 shares. Other inside purchasers include Richard House, who bought 48,000 shares for $60,000, and Scott King, who in March bought 25,000 shares for $44K.

Ascendiant analyst Theodore O’Neill sees a clear path forward for FPAY. He writes, “We believe the current horrendous macro-environment could be a big positive for FPAY. Looking at recovery from the last great recession, and in particular looking at the stocks of companies that sell tires and mattresses, where FPAY has good exposure, those stocks rose 2x-3x off the bottom in the first year… We believe the addressable market for FPAY is at least $25 billion. The market is for sub-prime borrowers and those without access to conventional credit, however it isn’t limited to that segment and could diversify further.”

O’Neill gives FPAY a $5 price target, implying an upside of 203% for the coming year. (To watch O’Neill’s track record, click here)

There are only two reviews on record for FPAY shares, but both are Buys. The stock’s trading price is $1.65 and the average price target is $4.25, which shows the rich potential in penny stocks – the upside here is an impressive 151%. (See FlexShopper analyst ratings on TipRanks)

Saratoga Investment Corporation (SAR)

Next up is an investment management company. Saratoga inhabits the mid-market private investment segment, putting capital into debt, appreciation, and equity investments. The company’s income comes from interest, dividends, and appreciation. As of the end of fiscal 2020, Saratoga had over $487 million in assets under management, with a varied portfolio including home security, industry, software, and waste disposal.

Saratoga reported 61 cents per share in its most recent quarterly, matching the results from calendar Q4 2019. The company’s shares are down 44% in the overall bear market, serious underperformance compared to the S&P 500. At the same time, quarterly net investment income was up 21% to $58.44 million. The company did defer its dividend payment in the current quarter – not a positive move, but a cautious play that maintains cash reserves in a time of crisis.

The insiders, however, clearly like this stock. Over the past three weeks, CEO Christian Oberbeck, CFO Henri Steenkamp, and board member George Cabell Williams have all made sizable purchases. Oberbeck’s buys have totaled over $320,000, which he spent on 24,000 shares. Williams bought 12,000 shares for $154,000, and Steenkamp picked up 2,000 shares for $26,000. These purchases have put a positive spin on the SAR’s insider sentiment.

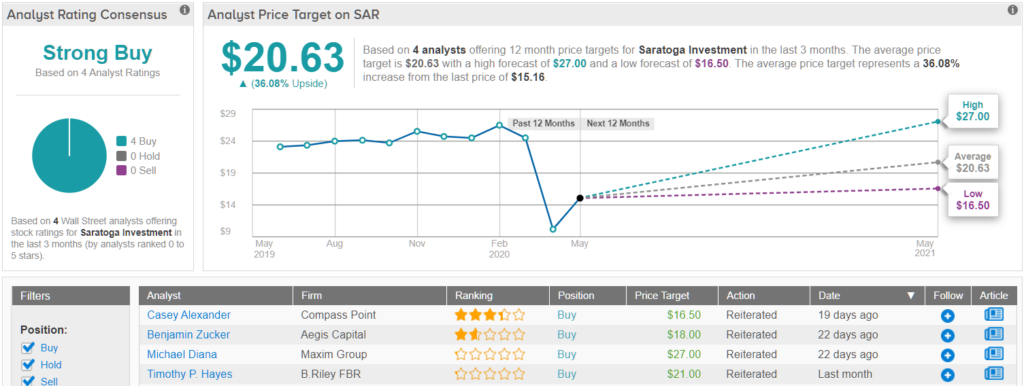

Analyst Timothy Hayes, of B. Riley FBR, reiterated his Buy rating and maintained his $21 price target on the stock. His target implies a robust upside of 36% in the coming 12 months. (To watch Hayes’ track record, click here)

Backing his rating, Hayes noted the serious move to defer the dividend: “…we believe SAR is being overly conservative with the decision, and is aiming to preserve as much liquidity as possible in anticipation of bear case scenarios. We do not view the dividend deferral to reflect a deterioration in credit or earnings power, as nonaccruals remain low (as of May) and we believe SAR received all scheduled interest payments in April.”

Overall, the stock has a unanimous Strong Buy analyst consensus rating, based on 4 reviews. The share price, $15.20, is an attractive point of entry for an equity with a $20.63 average price target; that indicates room for 36% upside growth this year. (See Saratoga stock analysis on TipRanks)

Selective Insurance Group (SIGI)

Investing legend Warren Buffett has long been known as a fan of insurance companies. He likes them for their ‘float,’ the money they take in from premium payments and hold until needed – and which they can use to generate investment profits in the interim. Selective Insurance Group is a holding company, controlling “A”-rated subsidiaries in the Property and Casualty sector. The company operates in 27 states, in the Southwest, Midwest, Northeast, and Southeast, along with Washington, DC.

In recent weeks, two company directors, William Rue and Terrence Cavanaugh, have made large share purchases in their company. Cavanaugh’s, the smaller of the two, totaled 1,000 shares, at a disclosed price of $46,020. Rue’s purchase was significantly larger; he picked up 25,000 shares for $1.3 million, making his total holding in SIGI over $21 million. Both purchases are considered informative, and have swung the insider sentiment on SIGI sharply positive, above the sector average.

SIGI has plenty to offer investors. While shares have underperformed in the current market environment, and are down 22% since the cycle changed back in February, the company’s earnings have remained positive. Selective reported 84 cents EPS in Q1. While that missed the forecast, the company’s revenues grew year-over-year, reaching $709.5 million.

JMP Securities analyst Matthew Carletti believes “Selective’s reserves are well situated in totality, certain areas, such as commercial auto and E&S lines, have seen additions in recent periods.”

Carletti reiterated a Buy rating on the stock along with a $65 price target, which implies room for a healthy 22% upside potential this year. (To watch Carletti’s track record, click here)

Overall, the analyst consensus rating on SIGI shares is a Moderate Buy, based on a mix of 2 Buys and 3 Holds. Shares are selling for $53.45, and the average price target, at $54.20, far more than cautious that Carletti’s – it suggests a minimal 1.4% upside from current levels. (See SIGI stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.