The S&P 500 has broken above 3,000, marking a milestone in the current bull rally. There’s a deepening feeling that equities by be a leading indicator, showing that the economy will turn around in 2H20.

That’s the blue-sky scenario, and it may happen. We live in an uncertain world, however, and even the most upbeat investors will look for ways to defend their portfolio in times like these. It’s natural to look at value stocks, equities trading at low cost but offering high upside potential, and high-yield dividend stocks, with their steady income stream providing a cushion against share depreciation. We’ve used TipRanks database to find three stocks to fit that profile.

Ares Commercial Real Estate (ACRE)

We’ll start with a real estate investment trust. These companies typically pay out high yield dividends, as tax codes require them to return a high percentage of income directly to shareholders. Ares, which originates, invests in, and manages commercial real estate loans in the mid-market, is typical of its niche.

The economic and market slides of the past few months hit the company hard. With commercial activity slowing, there were fewer opportunities for real estate loans, and repayment income was hit. Ares saw a sequential decline in earnings from Q4 to Q1, although at 11% it was not as deep as many similar companies. The company’s stock price is still down, however; with a net share price loss of 50%, Ares has badly underperformed in the current cycle.

Even though the stock is down and income is lower, Ares has maintained its solid dividend. The company paid out 33 cents per share in Q1, slightly more than its EPS. The yield, however, is the true attraction here – at 16.5%, it is sky-high, far higher than the 2.2% average found among peer companies in the financial sector.

JMP’s 5-star analyst Steven DeLaney sees ACRE’s current condition as an opportunity to buy in at lower prices. He writes of the stock, “…our outlook for a recovery in the value of ACRE shares remains positive after an expected few months of temporary economic turbulence as the company has minimal exposure to higher-risk commercial property types and has generally demonstrated solid loan underwriting since its inception in 2012.”

DeLaney’s Buy rating is backed by a $10 price target, suggesting room for a robust upside of 32%. (To watch DeLaney’s track record, click here)

Ares has a unanimous Strong Buy analyst consensus rating, based on 3 recent Buy reviews. Shares are selling for $7.61 and the average price target matches DeLaney’s at $10. The 31% upside and ultra-high dividend yield should bring investors in. (See ACRE stock analysis on TipRanks)

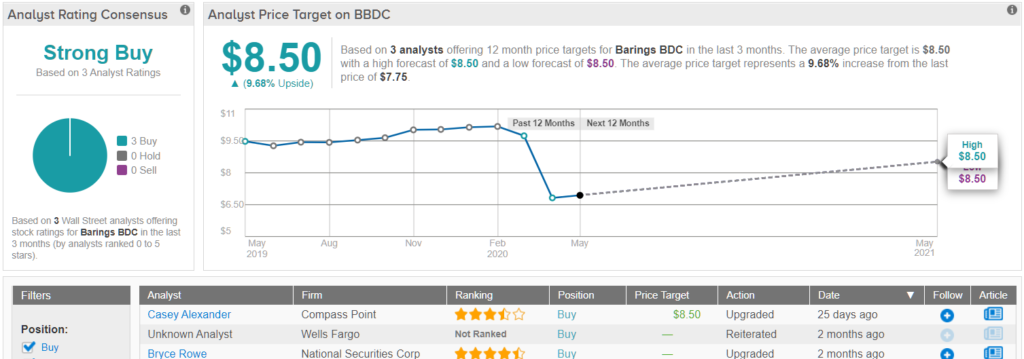

Barings BDC, Inc. (BBDC)

Next up is a business development corporation, Barings BDC. This company, provides asset management and direct origination for its customers to raise capital. Barings invests in middle market debts, equities, and fixed income assets, with customers around the world. Barings boasts over $327 billion in world-wide assets under management.

In Q1, Barings managed to avoid sharp sequential declines, but the 15-cent EPS still missed the forecast by a penny. Top line revenue, at $18.7 million missed the forecast by almost 2%; however, it did show modest year-over-year growth.

BBDC pays out 16 cents per share quarterly, making the yield on the 64-cent annualized payment an impressive 9%. While not as stellar as Ares above, it is still more than 4x higher than the average 2% yield found among S&P listed companies.

Finian O’Shea covers this stock for Wells Fargo and writes, “With a stable portfolio, leverage and liquidity profile, we believe BBDC is one of the names that will sail through the recession with comparatively little harm – and therefore likely to provide a very attractive return over the medium to long term.” (To watch O’Shea’s track record, click here)

The Strong Buy analyst consensus rating here is another unanimous vote, also based on 3 reviews. BBDC is selling for $7.40 per share, and the average price target of $8.50 indicates room for a 10% upside potential. (See Barings BDC stock analysis on TipRanks)

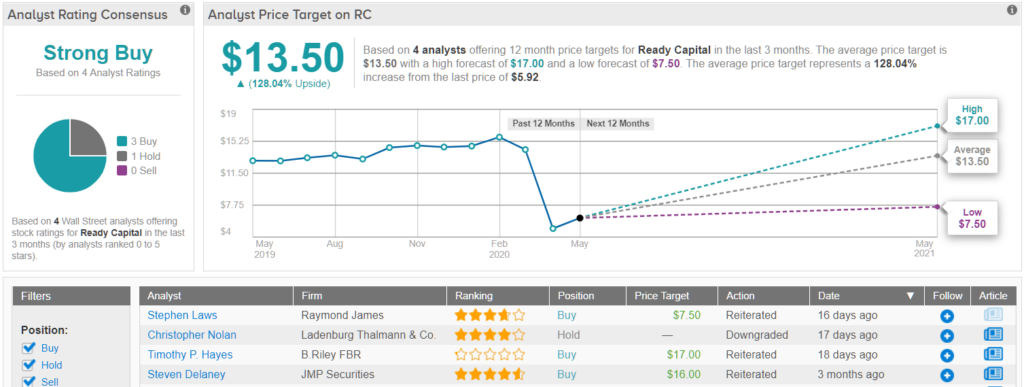

Ready Capital Corporation (RC)

Last up is another REIT, this one focusing on commercial mortgages. Ready Capital buys, originates, finances, and manages loans for commercial mortgages and related real estate securities including multi-family properties. The company’s customer base is in the US, where it boasts that it has provided over $3 billion in capital through its services.

Ready suffered the worst share price loss of the stocks in this list, as it is down 59% since February. Shares have been flat since their initial decline, and the first quarter saw earnings collapse from over 40 cents to just one penny.

However – the prospect for Q2 is better, with forecasts predicting up to 52 cents EPS inQ2. Most investors appear to see Ready’s pain as already baked in – repayments were down, but as the economy improves that situation is likely to reverse itself. In the meantime, Ready has kept up its dividend at 40 cents quarterly. The annualized payment is $1.60 per share. These are decent numbers, but the yield is where it’s at here. RC’s dividend yields an eye-popping 25% after the share declines – more than enough to make the potential risks worthwhile.

Piper Sandler analyst Crispin Love writes, “We believe RC can weather the volatility given its diversified platform, low LTVs, PPP benefits, and potential to buy distressed assets in 2020/2021… The company’s $4.2B portfolio of 4,500 loans have LTVs of about 60% and 90% of loans are current through April 30. In the CRE portfolio, 10% of loans are in forbearance while 7% of loans in the resi portfolio are in forbearance. Given RC’s focus on small balance, we believe there were worries that forbearance rates would be significantly higher.”

All of this is a recipe for a stock ready to bounce back, and Love rates RC a Buy. The analyst’s $17.50 price target shows how strong his confidence is – it implies an upside potential of 195% for the coming year. (To watch Love’s track record, click here)

While RC shares get another Strong Buy from the analyst consensus, also based on 3 Buy reviews, there is some caution here, shown by one Hold tossed into the mix. Ready’s shares are selling for $5.92, and the average price target of $13.50 suggests a strong upside of 128%. (See Ready stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.