Tony Anderson | DigitalVision | Getty Images

Some people will do just about anything to buy their first home.

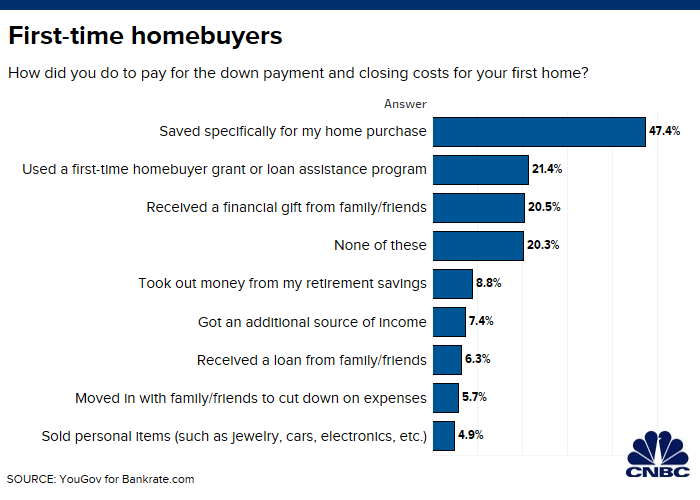

Just under 10% of homeowners surveyed by Bankrate.com, a personal finance website, said they took out money from their retirement savings to help cover the down payment and closing costs on their first dwelling.

The site polled a total of 2,582 adults from July 31 through Aug. 2.

Nearly half saved money specifically toward their home purchase, while another 20% said they received a financial gift from family and friends.

The median sales price for a home is $320,300, according to the Federal Reserve Bank of St. Louis, which can make the recommended down payment of 20% — what you’ll need to avoid the additional cost of private mortgage insurance — a heavy lift for new buyers.

Millennials are more likely than Gen Xers to use their retirement savings and sell personal belongings to scrape up the money, the survey found.

“It’s troubling that people feel like they have to tap into their retirement savings,” said Deborah Kearns, mortgage analyst with Bankrate. “

They’re already not saving enough for retirement, and they’re compounding the problem by taking out a loan or not contributing to save for a down payment,” she said.

Tapping your 401(k)

How you tap your retirement account matters.

If you decide to withdraw the down payment from your 401(k), the distribution is subject to a 20% withholding for taxes. You’ll also face a 10% penalty tax if you’re under 59½.

Borrowing can also be harmful. If your employer allows 401(k) loans, you’ll need to meet certain criteria in order for the amount you borrow to be tax-free.

In that case, you’re limited to a maximum of 50% of your vested account balance or $50,000, whichever is less.

Whether you withdraw the money in your retirement plan or you take out a loan, the cash you’re using is no longer benefiting from compound interest and market growth.

401(k) loan traps

Westend61 | Westend61 | Getty Images

Generally, you must repay your 401(k) loan within five years and make substantially level payments at least quarterly.

However, if you’re borrowing for your principal residence, you may take more time to repay it.

You’re also paying interest on that 401(k) loan, even though you’re essentially paying yourself back.

If you leave your job while you have an unpaid 401(k) loan on the books, you may have until the due date of your federal income tax return, including extensions, to roll over the amount owed to an IRA or another 401(k) plan.

You’re still on the hook to pay what you owe. If you fail to repay it, the balance can be treated as a taxable distribution.

Managing upfront costs

About 20% of the participants in the Bankrate survey said that they used first-time home buyer programs to help cover their down payment.

Here’s where to star for that.

Research home-buyer assistance programs: Loans through the Federal Housing Administration, the U.S. Department of Agriculture and the Department of Federal Affairs require low or no down payment. Borrowers may also be able to qualify with less-than-sterling credit.

Borrow responsibly. Don’t borrow the maximum that a bank is willing to offer. “Just because the lender says you qualify for X in loans, doesn’t mean you need to take that full amount,” said Kearns.

While banks are looking at your credit report items to assess your debt levels, they aren’t necessarily thinking about your monthly cash flow. “Lenders aren’t looking at your daycare bill,” Kearns said.

More from Personal Finance:

Half of student borrowers worry they’ll be in debt forever

Your kids don’t think your money skills measure up

What Trump’s call for 0% interest rates mean for you

Housing costs, including principal and interest payments on your mortgage, as well as taxes and insurance, should account for no more than 28% percent of your gross monthly income.

This so-called “front-end ratio” is a rule of thumb among lenders and financial planners.

Plan for higher costs. The struggle to save for the down payment is only part of the battle. Don’t forget the cost of maintenance once you’ve bought your home.

“Homeownership is so much more than just the mortgage payment,” said Kearns. “Higher utility bills are likely, and you have the repairs and elbow grease that go into it.”