Panoramic Images | Getty Images

Many global investors are turning toward Silicon Valley instead of Wall Street in search of returns.

The total invested in private markets hit all-time highs last year and continues to break multi-decade records this year. In the first half of the year, total investments in venture capital hit a 19-year high of $53.3 billion, according to data from Refinitiv published last week. That marked a 21% increase by total dollar amount compared to the first half of 2018.

The steady stream of funding comes alongside a drop in the number of publicly listed companies, rock-bottom global bond yields, and historically weak small-cap performance.

“The incentives for early exposure to rapidly growing, mature companies are still intact,” Pitchbook senior manager Garrett James Black said in the firm’s 2019 “Unicorn Report” published Monday. “With those imperatives in place and current market conditions — despite concern about a supposed imminent recession— looking to persist, unicorns aren’t going away anytime soon.”

Analysts say the trend is largely the result of relatively lower expectations for Wall Street investments such as stocks or bonds. As the trade war between the U.S. and China escalates and economic indicators weaken, investors have fled to safer assets such as Treasurys. The 10-year Treasury note fell below 1.7% Monday.

‘Starved for returns’

Money managers for pensions and endowments are turning to alternative investments — private equity, venture capital or hedge funds – to “keep up with expectations that they set years ago with their stakeholders,” according to McKinsey Partner Bryce Klempner.

“In a world where big institutional investors find themselves starved for returns, it’s not surprising that they have steadily increased allocations to private markets and you’ve seen capital continuing to flow into the asset class,” Klempner told CNBC in a phone interview. “Private equity has, on average, managed to outperform public markets over the last couple of decades.”

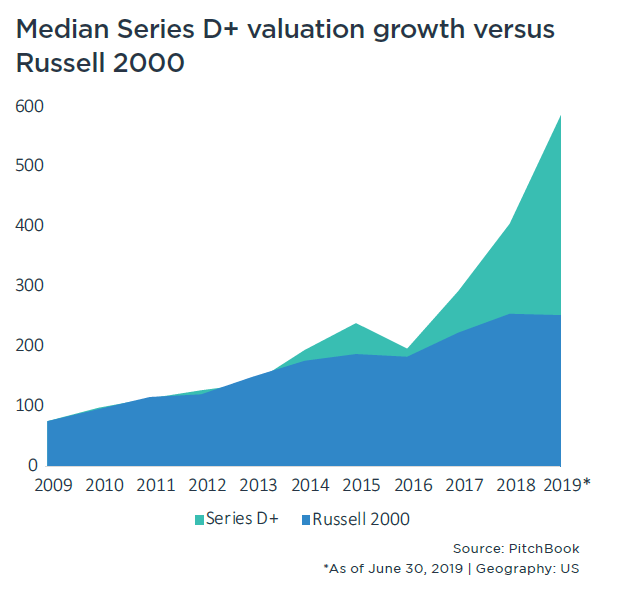

Growth in smaller public companies has been significantly slower than their private-market counterparts. PitchBook looked at the valuations of late-stage, Series D funded companies compared to the small-cap benchmark Russell 2000. That index is in correction territory, trading nearly 14% below its 52-week intraday high in August of 2018. The S&P 500 is off by 4% from its high.

Meanwhile, there has also been a contraction in the total number of public companies. Part of that is due to mergers and consolidation, but Klempner said managers — not just investors — tend to prefer private ownership, too. They’re able to operate “outside of the quarterly spotlight or the glare of public markets,” and often take a longer-term view, he said.

“As a consequence, you’ve seen considerable management talent migrate to private equity portfolio companies,” Klempner said.

One factor allowing companies to stay private was a change in legislation. The 2012 JOBS Act raised the limit of private shareholders in a company from 500 to 2,000 – meaning companies can stay private until they reach that limit. And in many ways, companies don’t need to go public: They can raise money with ease from private investors and don’t need the cash injection that comes with an initial public offering.

Foreign buyers

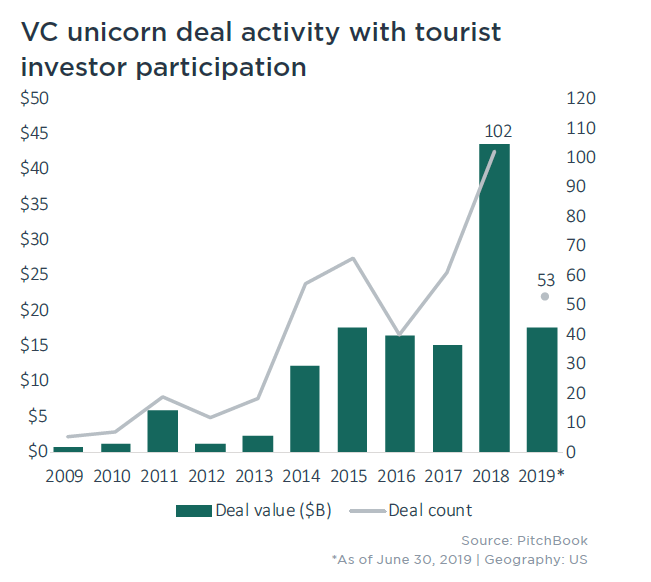

Foreign investors are also looking for early entrance into quickly growing tech companies, which in the case of Uber and WeWork, stayed off of public stock exchanges for a decade. Last year, venture capital deals that included “tourist” investors soared to more than $45 billion over 102 investments. Halfway through 2019, the deal total was at 53.

Another factor fueling the growth in private equity is acceptance and usage of secondary markets for investors to get liquidity. In traditional stock markets, it’s easier to buy and sell your stake with the click of a button or calling your broker. And there are plenty of buyers on the other side.

With private markets, that’s not always the case. Private companies aren’t listed on exchanges, meaning finding a buyer isn’t as seamless since alternative assets are mostly off limits unless you’re a qualified, or accredited investor.

“It’s important to emphasize that multiple companies are now increasingly comfortable buying and selling the securities of large, privately held companies in private transactions at the scale of billions of dollars,” Pitchbook’s Black said in the report.

McKinsey’s Klempner called it a snowball effect. As secondary markets get deeper, the extent of the discount investors would need to sell a stake in a privately owned company is much less painful than it was a few years ago.

“For a long time, some investors were relatively wary of private markets because of the perceived illiquidity of those asset classes,” he said.

Despite the shift, Klempner highlighted the sheer size of public markets — $70 trillion, versus about $5 trillion in total assets under management for private equity — as a sign that stock markets are here to stay.

Still, some analysts have pointed to potential negative effects in the shift to private markets. There is potential for less liquidity in public markets, causing more volatility, and retail investors may have fewer high-growth opportunities as companies opt out of listing on exchanges.

“It throws a spotlight on the resilience of the liquidity of public markets and even questions the point of a public stock market,” Bernstein senior analyst Inigo Fraser-Jenkins said in a note to clients in May. “Soon, active investing is going to be mainly in private markets.”

Fraser-Jenkins also highlighted the difficulty of the average stock market investor to get exposure to high-growth companies until they list on public exchanges.

“This should be a concern for policymakers, as the public equity market allows for democratized access to investment vehicles in a way that private assets do not,” Bernstein’s Fraser-Jenkins said.