Wall Street analysts say it is increasingly possible the Trump administration will try using a stronger weapon in the currency wars than just presidential tweets and rhetoric about unfair foreign central banks and currency manipulation.

Analysts now say there is a chance, albeit slim, that the Trump administration could ‘intervene’ to weaken the dollar, which means the U.S. government would actually sell dollars and buy other currencies. But what they see as more likely is the U.S. will verbally abandon the long-standing strong dollar policy, in an effort to level what it sees as an uneven playing field with countries, like China, harming U.S. exporters with a weaker currency.

President Donald Trump has been complaining more frequently about the dollar and currency manipulation. For instance, on July 3, he tweeted that China and Europe have made policy moves to cheapen their currencies to compete with the U.S. and perhaps the U.S. should “match” the actions. He has also repeatedly criticized Fed policies, and he blasted European Central Bank President Mario Draghi last month for opening the door to more easing policy, which sent the euro lower.

Pimco’s Joachim Fels, in a note Monday, said the president and other administration officials have been more explicit about their interest in a weaker dollar, implying the U.S. could intervene in the market.

“Following a pause since early 2018, the cold currency war that has been waging between the world’s major trading blocs for more than five years has been flaring up again. Moreover, even an escalation to a full-blown currency war with direct intervention by the U.S. and other major governments/central banks to weaken their currencies, while not a near-term probability, can no longer be ruled out,” wrote Fels, Pimco global economic advisor.

While market speculation has been rising about an intervention, the dollar ironically could be in for a period of decline, in part because the Fed has moved to an easing policy and is expected to cut interest rates.

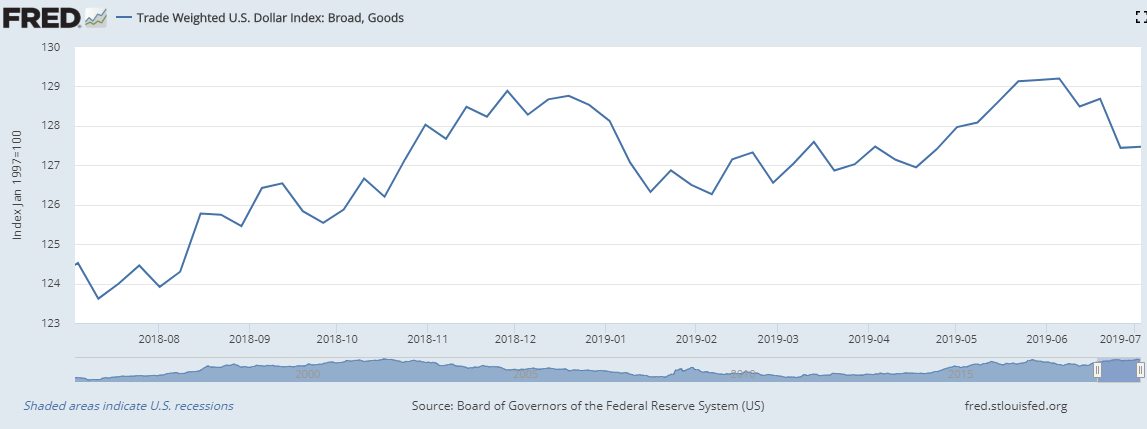

Marc Chandler, chief market strategist at Bannockburn Global Forex, said dollar volatility is at a multi-year low, and the dollar has been in a fairly narrow range. The broad trade-weighted dollar, a measure of the currency against a broad group of trading partners, has been falling.

“Interest rates have been narrowing,” said Chandler, noting the U.S. Treasury yields are getting closer to German, U.K. and Japan. “That’s a sign of the last phase of the dollar’s rally.”

Chandler doubts there will be an intervention. “Other countries are ignoring it. It takes two to tango,” he said.

Strategists from both Bank of America Merrill Lynch and Goldman Sachs said last week that intervention risks are low but rising. The Goldman analysts said the discussions about currency policy “comes against a backdrop where the “President has surprised investors on trade policy issues, which has created a perception that ‘anything is possible.'”

“While this would cut against the norms of recent decades, developed market central banks have recently used their balance sheets more actively, and FX intervention is akin to unconventional monetary policy, at least in an operational sense,” Goldman analysts noted.

Ben Randol, G-10 foreign exchange strategist at Bank of America Merrill Lynch, said the risk of the U.S. intervening should not be ignored, but he expects the administration to use words more than action.

The ‘strong dollar policy,’ instituted by former Treasury Secretary Robert Rubin during the Clinton administration, has been given lip service by subsequent administrations since, but it could be abandoned.

“We’re also looking at (National Economic Council Director) Larry Kudlow saying ‘we want a stable dollar,’ not a stronger dollar. He seems to be backing away from that,” said Randol. “I think they’re beginning to change the way they’re describing policy and not using the word ‘strong.'”

Randol said there are some comments that indicate the administration may be considering an intervention, which he believes is not likely.

“The dollar is about 10% or more overvalued relative to its long term equilibrium. The Treasury is beginning to sight those (IMF) studies as well,” he said. “We think that’s an important sign that the administration is looking at the dollar and its long term competitiveness and that could be an inspiration or serve as a reason why they would want to intervene.”

He said G-20 countries have agreed not to conduct solo interventions, unless there is extreme currency volatility. He said the last intervention was a coordinated move to drive down the yen, when it was rising following the 2011 tsunami.

“Unless they really want to jettison decades of precedent, they can only intervene on the pursuit of stabilizing the dollar and not come out and say we’re targeting the level of the exchange rate. That won’t fly and by the way, they don’t have the fire power to back it up,” said Randol.

Randol said the Treasury instructs the New York Fed to carry out operations on the dollar, and the fund it would use has assets of $94 billion. There is $36 billion of cash and cash equivalents, with $22 billion in Treasurys.

“They could see those dollars into the market and buy foreign exchange,” he said. Randol said the Treasury uses the New York Fed to conduct operations and it would likely use just a couple of billion dollars if it were to intervene. “It’s small but it sends a signal.”

Randol said there is little chance other countries would agree to an intervention, just because the U.S. does not like the value of the dollar. So more likely is the U.S. would find a reason to act alone based on volatility.

“We need to be thinking about this. Anything is possible. What I’m closely monitoring is when the dollar rallies because of wobbly risk asset markets, and in that environment, the probability of intervention is much higher,” he said, noting a stock market sell off could trigger a sharp flight to safety in the dollar.