Municipals were mixed in secondary trading as large general obligation bond offerings from Illinois and New York City took the focus and saw yields lowered in repricings. U.S. Treasuries were better in a risk-off rally with the biggest gains 10 years and out while equities saw massive losses.

Municipal to UST ratios rose further on the 10- and 30-year as a result of the underperformance to taxables. Muni to UST ratios landed at 90% in five years, 104% in 10 years and 110% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 87%, the 10 at 99% and the 30 at 107% at a 4 p.m. read.

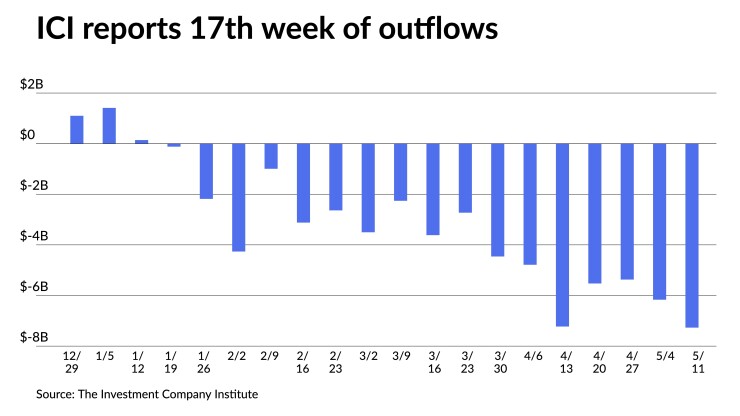

Wednesday marked the 17th week of outflows from municipal bond mutual funds, with the Investment Company Institute reporting investors pulled $7.270 billion from muni bond mutual funds in the week ending May 11 — the largest of 2022 so far. This is up from $6.167 billion of outflows in the previous week.

Exchange-traded funds saw another round of inflows at $1.756 billion versus $1.002 billion of inflows the week prior. Exchange-traded funds have seen $1 billion-plus inflows four times so far this year in a continued signal of crossover interest.

In the primary, Citigroup Global Markets priced and repriced for Illinois (Baa1/BBB+/BBB+/) $1.638 billion of general obligation bonds. The first tranche, $925 million of Series of June 2022A, saw 5s of 3/2023 at 2.81% (-9), 5s of 2027 at 3.78% (-1), 5s of 2032 at 4.40% (-2), 5.25s of 2037 at 4.64% (-2), 5.5s of 2042 at 4.72% (-2) and 5.5s of 2047 at 4.80% (-2), callable in 3/1/2032.

The first tranche, $713.375 million of Refunding Series of June 2022B, saw 5s of 3/2023 at 2.81% (-9), 5s of 2027 at 3.78% (-1), 5s of 2032 at 4.40% (-2) and 5s of 2036 at 4.69% (unch), callable in 3/1/2032.

BofA Securities priced for institutions $950 million of tax-exempt general obligation bonds, Fiscal 2022 Series D, for New York City, with saw yields lowered by up to six basis points inside 10 years and cuts of up to seven basis points on the long end from Tuesday’s retail offering: 5s of 2024 at 2.49% (-6), 5s of 2025 at 2.72% (-6), 5s of 2030 at 3.36% (-4), 5s of 2032 at 3.62% (unch), 5s of 2037 at 3.99% (+3), 5.25s of 2042 at 4.26%, 5.5s of 2046 at 4.21% and 4.5s of 2049 at 4.64% (+7), callable 5/1/2032.

BofA Securities priced for the East Bay Municipal Utility District, California, (Aaa/AAA//) $309.105 million of water system bonds. The first tranche, $133.860 million of green revenue bonds, Series 2022A, saw 5s of 6/2024 at 2.32%, 5s of 2027 at 2.67%, 5s of 2032 at 3.15%, 5s of 2037 at 3.55%, 5s of 2042 at 3.76%, 5s of 2047 at 3.87% and 5.25s of 2052 at 3.92%, callable 6/1/2032.

The second tranche, $72.025 million of revenue refunding bonds, Series 2022B-1, saw 5s of 6/2023 at 2.02%, 5s of 2030 at 3.02%, 5s of 2032 at 3.15% and 5s of 2037 at 3.55%, callable 6/1/2032.

The third tranche, $103.220 million of revenue refunding bonds, Series 2022B-2, saw 5s of 6/2023 at 2.02%, 5s of 2027 at 2.67%, 5s of 2032 at 3.15% and 5s of 2034 at 3.48%, noncall.

In the competitive market Wednesday, St. Louis County, Missouri, (/AA//) sold $123.605 million of convention center revenue bonds, Series 2022A, to Wells Fargo Bank, with 5s of 12/2034 at 3.71%, 5s of 2037 at 3.91%, 4s of 2042 at 4.30% and 4s of 2047 at 4.55%, callable 12/1/2030.

The market is dealing with “a new round of headwinds with a large new-issue calendar and ongoing heavy bids lists — creating yield clog and setting new levels across the curve,” said Kim Olsan, senior vice president at FHN Financial.

Bids wanted once again surpassed the $2 billion mark on Tuesday and Monday, she said, “bringing the total to five sessions this month where that has occurred and harkening back to the March 2020 period when 11 sessions saw similar par sizes.”

In primary market activity, she said that “high-grade spreads are a realization of the flipped demand scenario at work.”

She said Tuesday’s competitive sale of triple-A-rated Prince George’s County, Maryland GOs drew “a 5% 10-year maturity spread +18/AAA and the 5% due 2042 came +35/AAA — each about 10 to 15 basis points wide to more historical levels.”

Olsan noted that “negotiated results are proving out a similar theme with deal placement challenged along the curve.”

Gilbert, Arizona, priced triple-A-rated utility revenue bonds “with spreads of +31 to +47/AAA from 10 years and longer in 5% structures,” she said.

“A 20-year 4% was finalized at 4.40% — a stark contrast to comparable credits that came to market just a month ago more than 100 basis points lower in yield,” she said.

Illinois’ GO offering brought recalibrated couponing on the long end to 5.50%, up from 5.25% and a contrast to the state’s March 2021 pricing when the maximum coupon was 5% in longer maturities, Olsan noted.

While some of the best opportunities are available to buyers currently, she said sellers are “finding new yield ranges are required for orderly placement.”

Upcoming issuance, she said, can be expected “to see tailor-made structures come into play while the rate and inflation outlooks remain volatile.”

However, she said one positive is the net supply/reinvestment figure “sits at a projected negative $9 billion in the next 30 days, with both New Jersey and California placed in the largest negative supply scenarios.”

“This year’s yield moves have had unique effects on the credit curve,” Olsan said. “Whereas 2021’s trade was long in maturity and lower in yield for maximum concession, this year’s preferences show reactions to current market conditions.”

All spot levels “show bidders’ adjustments to yield expectations for credits” outside the triple-A range, she said.

Olsan noted that “credit paring has come into play in recent bid-list activity as sellers look to lock in current levels before the end of the quarter.” In the 5-year range, she said, double-A revenues are trading nominally higher against triple-As but single-A-rated revenues have widened 27 basis points to triple-As from the end of 2021.

“Rates that ended in December well below 1% are now in the mid-2% area, with taxable equivalent yields increasing from below 1% to near 4% for 37% bracket buyers,” she said.

“Intermediate revenue bonds have adjusted more broadly” versus triple-A GOs, “with material absolute yield improvements as well,” Olsan said. From the end of 2021, she said 10-year double-A revenues “carry implied spreads that are 18 basis points higher” while single-A revenues are trading “nearly 50 basis points wider.”

“Real yield corrections in that timeframe exceed 200 basis points, translating into [taxable equivalent yields] now above 6% in some cases,” she said.

Additionally, she said that “long-end demand has shifted from last year’s trade, where up-in-coupon and up-in-credit trading is occurring.” In 20-year double-A revenue bonds, “spreads are tracking 37 basis points wider from the end of 2021 with yields above 3.50% (implied 5% coupons),” according to Olsan.

“Single-A revenues have widened out more than 50 basis points in the last five months, currently trading with yields well above 4%,” she said. “Depending on credit and coupons, TEYs are above 7%.”

Informa: Money market muni assets rise again

Tax-exempt municipal money market funds continued a four-week inflow streak as $2.27 billion was added the week ending May 16, bringing the total assets to $96.61 billion, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for all tax-free and municipal money-market funds rose 0.15% to 0.36%.

Taxable money-fund assets lost $9.37 billion to end the reporting week at $4.335 trillion in total net assets at $11.90 billion. The average seven-day simple yield for all taxable reporting funds rose 0.08% to 0.41%.

Banks unload munis

“U.S. banks’ exposure to municipal bonds and direct loans fell by a combined $11 billion” during the first quarter of 2022, the largest drop since the second quarter of 2019 and “representing a 1.7% contraction in banks’ muni risk portfolios,” said Matt Fabian, partner at Municipal Market Analytics.

He noted it is also the first quarterly decline in total bank holdings in 10 quarters.

The drop entails an $8 billion reduction in securities holdings and a $3 billion reduction in direct loans, which now total $416 billion and $195 billion, respectively, Fabian said.

“Because over half of the decline in bank securities portfolios reflect actions by very small bank holders of bonds, the changes appear to be more tactical (e.g., selling what is losing value) than strategic (e.g., making lasting reallocations away from munis),” he said, adding that banks are “still unlikely to pivot back into acquisitions as soon as the second quarter of this year.”

Secondary trading

New York City 5s of 2023 at 2.13%-2.12%. New York City 5s of 2024 at 2.62%-2.55%. New York City TFA 5s of 2024 at 2.53%-2.52%.

Georgia 5s of 2026 at 2.55%. Maryland 5s of 2026 at 2.57%. Minnesota 5s of 2026 at 2.57%. Georgia 5s of 2027 at 2.62%-2.61%.

Prince George’s County 5s of 2028 at 2.90%. California 5s of 2030 at 3.13%-3.12% versus 3.05%-3.04% Monday. Delaware 5s of 2031 at 2.98% versus 3.00% Tuesday.

New York Dorm PITs 5s of 2031 at 3.37%. New York City waters 5s of 2031 at 3.18%.

Boston 5s of 2034 at 3.10%-3.09%, the same as Tuesday. Washington 5s of 2039 at 3.69%-3.68%. Massachusetts Bay Area Transportation 5s of 2052 at 3.73%-3.72% versus 3.55%-3.50% Thursday.

AAA scales

Refinitiv MMD’s scale was cut unchanged at the 3 p.m. read: the one-year at 1.99% and 2.31% in two years. The five-year at 2.60%, the 10-year at 3.02% and the 30-year at 3.37%.

The ICE municipal yield curve saw one to two basis point cuts: 2.02% (unch) in 2023 and 2.37% (unch) in 2024. The five-year at 2.60% (+1), the 10-year was at 2.94% (+2) and the 30-year yield was at 3.341% (+2) at a 4 p.m. read.

The IHS Markit municipal curve was unchanged: 2.02% (unch) in 2023 and 2.32% (unch) in 2024. The five-year at 2.63% (unch), the 10-year was at 3.03% (unch) and the 30-year yield was at 3.37% (unch) at 4 p.m.

Bloomberg BVAL saw one to two basis point cuts: 2.02% (unch) in 2023 and 2.30% (unch) in 2024. The five-year at 2.66% (unch), the 10-year at 2.95% (+1) and the 30-year at 3.31% (+2) at a 4 p.m. read.

Treasuries rallied.

The two-year UST was yielding 2.670% (-3), the three-year was at 2.842% (-5), five-year at 2.891% (-8), the seven-year 2.916% (-9), the 10-year yielding 2.878% (-11), the 20-year at 3.254% (-14) and the 30-year Treasury was yielding 3.054% (-13) at the close.

Primary to come:

Memphis, Tennessee, (Aa2/AA//) is on the day-to-day calendar with $229.605 million of taxable general improvement refunding bonds, Series 2022B. J.P. Morgan Securities LLC.

The Indiana Finance Authority (Aa3/AA//) Is set to price on Thursday $134.355 million of CWA Authority Project first lien wastewater utility refunding revenue forward delivery bonds, Series 2022A, serials 2022-2042. Citigroup Global Markets Inc.

The Ohio Housing Finance Agency (Aaa///) is set to price on Thursday $130 million of mortgage-backed securities program residential mortgage revenue social bonds, 2022 Series B. J.P. Morgan Securities LLC.