Municipal secondary selling pressure remained elevated on bonds inside 10 years while the larger primary got underway and deals saw bumps in repricings as U.S. Treasuries made small gains and equities rallied.

Triple-A benchmark yields saw one to four basis point cuts while U.S. Treasuries ended the session better.

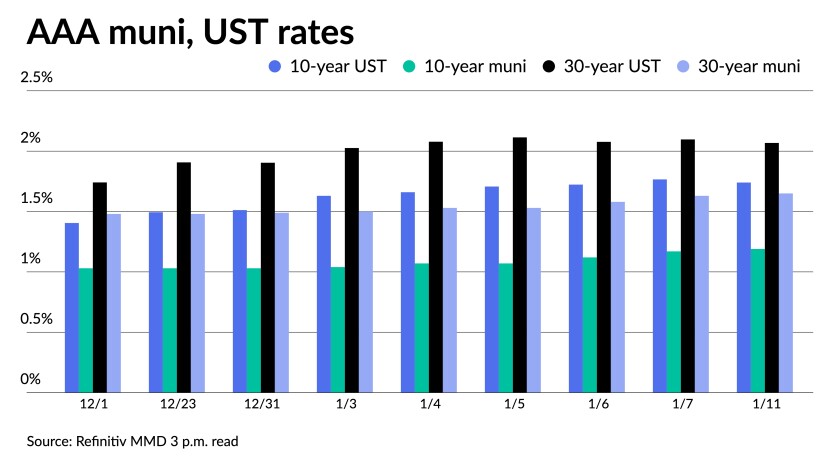

Municipal to UST ratios rose slightly on the day’s moves. The five-year was at 54%, 68% in 10 and 79% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 50%, the 10 at 70% and the 30 at 79%.

With the first day of a larger new-issue calendar, the primary took more of the focus Tuesday.

In the negotiated market, BofA Securities priced for the Virginia Small Business Financing Authority (/BBB/BBB/) $573.5 million of Elizabeth River Crossings Opco, LLC project forward delivery, alternative minimum tax senior lien revenue refunding bonds, Series 2022. Bonds maturing in 1/2029 with a 4% coupon yield 2.17%, 4s of 7/2029 at 2.21%, 4s of 1/2032 at 2.44%, 4s of 7/2032 at 2.48%, 4s of 1/2037 at 2.71% and 3s of 1/2041 at 3.25%, callable 1/1/2032.

BofA Securities priced for the Michigan Finance Authority (Aa3/AA-/AA-//) $264.04 million of Trinity Health Credit Group hospital revenue bonds. The first tranche, $202.135, Series MI 2022A, saw bonds maturing in 12/2028 with a 5% coupon yield 1.23%, 5s of 2032 at 1.56%, 5s of 2036 at 1.75%, 4s of 2027 at 2.22% and 2.75s of 2047 at 2.82%, callable 12/1/2031.

The second tranche, $61.905 million, Series MI 2022B, saw bonds maturing in 12/2043 with a mandatory tender date on 12/1/2028 with a 5% coupon yields 1.37%, callable 6/1/2028.

Raymond James & Associates priced and repriced for the Conroe Independent School District, Texas, (Aaa/AAA//) $162.01 million of unlimited tax school building bonds, Series 2022 with up to five basis point bumps. Bonds in 2/2023 with a 4% coupon yields 0.35% (-5), 5s of 2027 at 0.89% (-4), 5s of 2032 at 1.42% (-2), 2.5s of 2037 at 1.96% (-2), 3s of 2042 at 1.98% (-2) and 2.65s of 2042 on par, callable 2/15/2032.

Piper Sandler & Co. priced and repriced for the New Braunfels Independent School District, Texas, (/AAA//) $132.12 million of unlimited tax school building and refunding bonds with as much as five basis point bumps, Series 2022. Bonds in 2/2023 with a 5% coupon yields 0.36% (-4), 5s of 2027 at 0.93%, 4s of 2032 at 1.44%, 2.5s of 2037 at 1.96%, 3s of 2042 at 1.98% (-5) and 2.75s of 2049 at 2.70%, callable 2/1/2031.

In the competitive market, the Louisville and Jefferson County Metropolitan Sewer District in Kentucky (Aa3/AA//) sold $225 million of green sewer and drainage system revenue bonds to J.P. Morgan Securities LLC. Bonds in 5/2022 with a 4% coupon yields 0.38%, 5s of 2027 at 0.95%, 5s of 2032 at 1.4%, 4s of 2036 at 1.7%, 3s of 2042 at 2.13%, 2.625s of 2046 at 2.64% and 2.7s of 2052 on par, callable 5/15/2032.

The Iowa Board of Regents sold $201.755 million of University of Iowa hospital revenue bonds to Citigroup Global Markets Inc. Bonds in 9/2022 with a 5% coupon yield 0.37%, 5s of 2027 at 1.09%, 5s of 2032 at 1.58%, 4s of 2037 at 1.93%, 2.375s of 2042 at 2.48%, 2.6s of 2047 at 2.65% and 2.75s of 2051 at 2.70%, callable 9/1/2032.

The Iowa Board of Regents also sold $101.38 million of hospital revenue bonds to BofA Securities. Bonds in 9/2052 with a 3% coupon yield 2.80%, 3s of 2056 at 2.90% and 3s of 2061 at par, callable 9/1/2032.

Goldman Sachs released a preliminary pricing wire for the Board of Education of the City of Chicago‘s (/BB/BB+/BBB/) $862.65 million of dedicated revenue bonds. It showed the first tranche, $500 million of unlimited tax general obligation bonds, with bonds maturing in 12/2042 with a 4% coupon at 2.68% and 4s of 2047 at 2.80%, callable 12/1/2031.

The second tranche, $362.65 million of unlimited tax general obligation revenue bonds, saw bonds maturing in 12/2022 with a 4% coupon yield 0.73%, 4s of 2035 at 2.44%, 4s of 2037 at 2.53% and 4s of 2041 at 2.65%, callable 12/1/2031.

The New York City Transitional Finance Authority said Tuesday it will offer about $1.2 billion of future tax secured subordinate bonds next week. Proceeds will be used to fund capital projects.

The deal is composed of $950 million of tax-exempt fixed-rate bonds and $250 million of taxable fixed-rate bonds. J.P. Morgan Securities is expected to price the tax-exempts on Jan. 20, after a two-day retail order period starting on Tuesday. The TFA expects to competitively sell around $250 million of the taxables on Jan. 20.

Secondary trading

Ohio 5s of 2023 at 0.42%. Wisconsin 5s of 2023 at 0.39%. San Francisco City & County 5s of 2023 at 0.35%.

New York State Urban Development Corp. 5s of 2024 at 0.58%. Georgia 5s of 2025 at 0.61%.

Montgomery County, Maryland, 5s of 2026 at 0.84%. NYC water 5s of 2026 at 0.75%-0.72%. Ohio common school 5s of 2026 at 0.84%-0.83% versus 0.66%-0.64% Thursday.

Illinois Finance Authority 4s of 2027 at 0.92%. Dormitory Authority of the State of New York 5s of 2028 at 1.10%. Charleston County, South Carolina, 5s of 2029 1.12% versus 0.96% a week ago.

District of Columbia 5s of 2035 at 1.40% versus 1.27% a week ago. Washington 5s of 2040 at 1.68%. Ohio 5s of 2040 at 1.60%-1.58% versus 1.57% Monday and 1.56% Friday. California 5s of 2041 at 1.66%.

New York City water 5s of 2044 at 1.85% and 5s of 2048 at 1.92%. NYC TFA 4s of 2048 at 2.00% versus 2.01%-1.99% on Thursday.

AAA scales

Refinitiv MMD’s scale saw a four-basis point cut on bonds in 2025-2027, a three basis point cut in 2028, one basis point in 2029 and unchanged thereafter at the 3 p.m. read: the one-year at 0.33% and 0.50% in two years. The 10-year at 1.19% and the 30-year at 1.65%.

The ICE municipal yield curve showed yields rise by one to three basis points: up one to 0.31% in 2023 and up three to 0.50% in 2024. The 10-year was up one to 1.22% and the 30-year yield up one to 1.65% in a 4 p.m. read.

The IHS Markit municipal analytics curve was cut by one to three basis points: 0.34% (+3) in 2023 and 0.45% (+3) in 2024. The 10-year at 1.19% (+1) and the 30-year at 1.67% (+1) as of a 4 p.m. read.

Bloomberg BVAL was saw one to three basis point cuts to scales: 0.33% (+1) in 2023 and 0.47% (+3) in 2024. The 10-year at 1.22% (+2) and the 30-year at 1.66% (+1) at a 4 p.m. read.

Treasuries were steady while equities ended in the black.

The five-year UST was yielding 1.504%, the 10-year yielding 1.740%, the 20-year at 2.121% and the 30-year Treasury was yielding 2.068% at the close. The Dow Jones Industrial Average was up 183 points, or 0.51%, the S&P gained 0.92% while the Nasdaq was up 1.41% at the close.

Powell hearing

While other Federal Reserve officials have stated they would support a March liftoff, Federal Reserve Board Chair Jerome Powell would not commit to timing, stressing decisions would be data-based and the Fed will not allow inflation to become entrenched.

“We’re going to have to be humble and nimble,” Powell told the Senate banking committee during his nomination hearing. While he expects inflation to subside after midyear, he said, if it sticks around longer “monetary policy will have to adapt.”

He expects liftoff this year and balance sheet runoff but offered no specifics on timing. “Rate hikes will depend on data,” he said.

Answering questions about whether the Fed should be involved in addressing climate change or racial equity issues, Powell said, “We have to focus on the job Congress has given us.” He explained, “Climate is appropriate for us as an issue to the extent it fits within our existing mandates. The broader answer to climate change has to come from legislators and the private sector.”

The balance sheet runoff will start earlier this time, Powell said, since “the economy is in a completely different place than it was when we ended asset purchases the last time. Plus, with a bigger balance sheet than last time, he said, “the runoff can be faster.”

Officials are debating options and it could take up to four meetings to make a decision.

“Wall Street now has a better understanding on how the Fed will normalize policy and with the balance runoff likely taking up to four meetings,” said Edward Moya, senior market analyst at OANDA. “After Powell’s testimony, some investors feel they got the all-clear signal to buy the dip. The Fed’s window for tightening is complicated given inflation could finally peak during the summer and since they may not want to look political and be too aggressive removing accommodation so close to the midterm elections.”

While his statements could not be interpreted as “overly hawkish,” Moya said, Powell “paved the way for a lengthy debate over balance sheet reduction, with his normalization comments taking away some of the importance over [Wednesday]’s hot inflation report.”

The confirmation of Powell “would prove a welcome source of stability in an otherwise unstable world,” said Morning Consult Chief Economist John Leer. “Powell’s views of the economy are not particularly dogmatic, and he’s consistently voiced his commitment to following the data. … Additional experience from a veteran central banker like Powell would go a long way towards helping markets right now.”

Separately, Federal Reserve Bank of Kansas City President Esther George said, “With inflation running at close to a 40-year high, considerable momentum in demand growth and abundant signs and reports of labor market tightness, the current very accommodative stance of monetary policy is out of sync with the economic outlook.”

Even with tapering, she said, the balance sheet will continue to grow until the purchases end in March. “Removing accommodation will unavoidably be complicated by the use of multiple policy instruments — short-term rates and large-scale asset purchases — as it was during the last normalization cycle a decade ago,” George said. The size of the balance sheet and the long-term fed funds rate should be considered in the Fed’s decisions.

“My own preference would be to opt for running down the balance sheet earlier rather than later as we plot a path for removing monetary accommodation,” she said.

In conversations with Bloomberg News, Federal Reserve Bank of Cleveland President Loretta Mester and Federal Reserve Bank of Atlanta President Raphael Bostic spoke in favor of a March liftoff. Mester is an FOMC voter this year, Bostic voted last year.

Fitch Ratings now expects two rate hikes this year and four in 2023. Luigi Speranza, Chief Global Economist, BNP Paribas Markets 360 said BNP expects liftoff in March, with three additional rate hikes this year and four in 2023.

“Quantitative tightening will be announced in July, we think, brought forward from our previous base case of early 2023,” he said. “We expect monthly caps on balance sheet roll-off to start at $10 billion on both USTs and MBS ($20 billion total) and rise to $100 billion per month by December 2022 and target a balance sheet size of $6.2-6.9 trillion by end-2024.”

Primary to come

Louisiana (Aa2/AA-//) is set to price Thursday $651.035 million of taxable gasoline and fuels tax revenue refunding bonds, 2022 Series A. Wells Fargo Bank.

Comal Independent School District in Texas (Aaa//AAA/) is set to price Thursday $445.825 million of unlimited tax school building bonds, Series 2022, serials 2023-2047, insured by Permanent School Fund Guarantee Program. Raymond James & Associates.

The Los Angeles Department of Water and Power (Aa2//AA-/AA) is set to price Thursday $375 million of power system revenue bonds, 2022 Series A, serials 2027-2041, terms 2046 and 2051. Barclays Capital Inc.

Claremont McKenna College in California (Aa3///) is set to price Wednesday $300 million of corporate CUSIP taxable bonds, Series 2022. Morgan Stanley & Co.

Coast Community College District in Orange County, California, (Aa1/AA+//) is set to price Thursday $206.73 million of federally taxable 2022 general obligation refunding bonds, serials 2022-2037, term 2039. RBC Capital Markets.

California Municipal Finance Authority Special Finance Agency is set to price Wednesday $173.185 million of essential housing revenue bonds, consisting of $96.41 million of senior bonds, Series 2022A-1, term 2057 and $76.775 million of junior bonds, Series 2022A-2, term 2049. Jefferies.

The Rhode Island Housing and Mortgage Finance Corp. (Aa1/AA+///) is set to price Thursday $138.145 million of homeownership opportunity bonds, consisting of $124.345 million of non-alternative minimum tax social bonds, Series 76A and $13.8 million of federally taxable social bonds, Series 76-T. J.P. Morgan Securities.

Tomball Independent School District in Texas (Aaa/AAA//) is set to price Wednesday $127.39 million of unlimited tax school building bonds, Series 2022, serials 2023-2047, insured by Permanent School Fund Guarantee Program. RBC Capital Markets.

Cuyahoga County, Ohio, (/AAA//) is set to price Thursday $123.39 million of tax-exempt Sales tax revenue bonds, Series 2022A, for the Ballpark Improvement Project. KeyBanc Capital Markets.

Colby College (Aa2/AA/) in Maine is set to price Wednesday $100.7 million of corporate CUSIP taxable bonds. Barclays Capital.

New Mexico Mortgage Finance Authority (Aaa///) is set to price Thursday $100 million of tax-exempt, non-alternative minimum tax single family mortgage program Class I bonds, 2022 Series A, serials 2023-2034, terms 2037, 2042, 2047, 2052 and 2053. RBC Capital Markets.

Competitive:

Stoneham, Massachusetts, is set to sell $135.16 million of general obligation municipal purpose loan of 2022 bonds, at 11 a.m. eastern Wednesday.

Las Vegas Valley Water District (Aa1/AA//) is set to sell $288.49 million of general obligation limited tax water improvement bonds at 10:30 a.m. Wednesday.

The Port of Seattle (Aaa/AA-/AA-/) is set sell $94.645 million of taxable, limited tax general obligation and refunding bonds, Series 2022B at 11:30 a.m. Thursday. This issuer is also set sell $15.73 million of alternative minimum tax, limited tax general obligation bonds, Series 2022A at 11 a.m. eastern Thursday.