Municipals outperformed Treasuries as yields rose 10 basis points on the UST 10- and 30-year on talk of a potential stimulus deal and equities hit all-time highs.

Secondary trading held municipal yields steady while Illinois’ highway deal priced and re-priced five to nine basis points lower and New York City Municipal Water Authority offered bonds to retail. The New Jersey Transportation Trust Fund’s $1.5 billion deal is scheduled to price as soon as Wednesday.

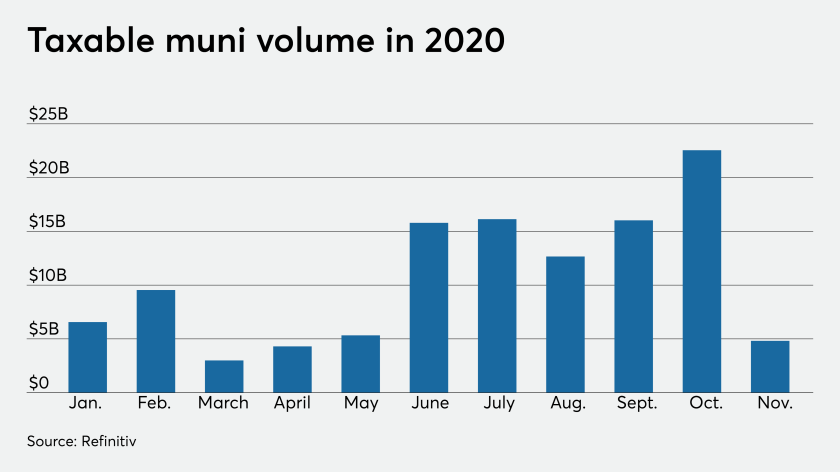

The dearth of November supply, including a precipitous drop in taxables during the month, coupled with hefty December redemptions/coupons, has led to municipal outperformance.

Municipals typically follow Treasuries, but not Tuesday. Munis are likely to lag Treasuries in some fashion once year-end empathy settles in mid-month and ratios become a factor, though 2020 has proven the muni/UST relationship has not been typical.

“But so far, munis feel firm like a rock,” a New York trader said.

Taxables are set to return near 10% on the year if the trend of increased issuance bleeds into this month and corporate bond issuance continues its lower volume.

Secondary trading of high-grades ticked up, with names such as North Carolina, Maryland, Georgia, D.C., Washington, California and others holding AAA benchmarks.

With generous supply expected this week and the upcoming visible supply, the municipal market is on track for a near record year in terms of gross supply, according to Peter L. Block, managing director of credit strategy at Ramirez & Co.

Strong market technicals, such as increased fund flows and November performance in sectors, like high yield, transportation, and dedicated tax are propping up the market, he noted.

Gross supply for the first week of December is estimated at $9.8 billion, while the 30-day visible net supply is negative $12.6 billion, reflecting $12.8 billion of announced supply against negative $25.4 billion of maturities and calls, Block said.

So far, gross supply year-to-date is $434 billion, an increase of 16.8% year-over-year, which includes $302 billion of tax-exempt and $133 billion of taxable.

“New-money issuance should be driven by pent-up infrastructure needs waylaid by the pandemic, whereas taxable bonds, issued primarily for tax-exempts refundings, should decline amidst a relatively smaller universe of candidates” to about $138 billion, Block wrote.

Block expects 2020’s total gross supply to be close to the record $448 billion set in 2017, with about $13 billion net supply and market growth.

Tuesday’s market tone follows on the heels of the Thanksgiving holiday week when municipals gained slightly, but outperformed Treasuries in 10 years and 30 years due to the combination of muted holiday activity and the Treasury selloff, Block noted.

Looking ahead, the firm’s 2021 municipal supply forecast projects minimal supply growth of less than 1% to $449 billion, driven by a 5.5% year-over-year increase in new-money tax-exempt bonds to $310 billion against a 20% decline in taxable bonds to $123 billion.

He assumes tax-exempt advance refundings remain prohibited and net supply is expected to grow to $109 billion in 2021 given the $100 billion decline of reinvestment versus 2020, according to Block.

Primary market

Siebert Williams Shank re-priced the Illinois State Toll Highway Authority’s (A1/AA-/AA-/) $500 million of Series 2020A toll highway senior revenue bonds.

The deal consisted of bonds in 2036 with a 5% coupon to yield 1.49% (-6 basis points in repricing), 5s of 2040 at 1.69% (-5) and 5s of 2045 at 1.87% (-9).

Siebert also priced for retail the New York City Municipal Water Finance Authority’s (Aa1/AA+/AA+/NR) $478 million of tax-exempt fixed-rate bonds. Price wires showed the deal in two series, the first, $249 million of water and sewer system second general resolution revenue bonds Subseries BB-1, 5s of 2050 to yield 1.74%, 3s of 2050 to yield 2.19%. The second, $229 million of water and sewer system second general resolution revenue bonds Subseries BB-2, priced to yield 0.23% with 4% coupon in 2023, 0.27% with a 4% in 2024, 1.75% with a 4% coupon in 2042.

BofA Securities priced $311 million of Denver Transit Partners Eagle P3 project exempt non-AMT and taxable PABs for the Regional Transportation District, Colo. (Baa2//A-/).

The exempt non-AMT PABs, $304 million, were priced to yield 0.65% with a 3% coupon in 2023 to 1.47% with a 5% coupon in 10-years and 2.44% with a 4% coupon in 2040 (noncall).

Citigroup Global Markets priced $133 million of general obligation bonds for the San Francisco Community College District for the City and County of San Francisco (Aa3/ /A+). Bonds maturing in 2022 with a 5% coupon yield 0.18%, 5s in 2023 yield 0.22% while 4s in 2045 yield 1.95%, 3s of 2045 yield 2.18% and 2.25s of 2045 yield 2.41%.

Still to come this week is the New York State Housing Finance Agency (Aa2/NR/NR/NR) with two deals totaling $483.44 million. JPMorgan Securities is set to price the $287.55 million of Series 2020L-2 climate bond certified affordable housing revenue sustainability and Series 2020M-2 sustainability bonds. Wells Fargo Securities is expected to price the $195.89 million of Series 2020L-1 climate bond certified/sustainability bonds and Series 2020M-1 affordable housing revenue bonds.

In the competitive arena, the Metropolitan St. Louis Sewer District, Mo., is selling $120 million of Series 2020B wastewater system revenue bonds on Thursday. PFM Financial Advisors and Independent Public Advisors are the financial advisors. Gilmore & Bell and White Coleman are the bond counsel.

Secondary market

High-grade municipals were little changed, according to final readings on Refinitiv MMD’s AAA benchmark scale. Short yields were flat at 0.14% in 2021 and 0.15% in 2022. The 10-year yield sat at 0.72% while the yield on the 30-year was 1.41%.

The 10-year muni-to-Treasury ratio was calculated at 85% while the 30-year muni-to-Treasury ratio stood at 89%, according to MMD.

The ICE AAA municipal yield curve showed short maturities unchanged at 0.15% in 2021 and 0.16% in 2022. The 10-year maturity also was unchanged at 0.71% with the 30-year at 1.43%.

The 10-year muni-to-Treasury ratio was calculated at 79% while the 30-year muni-to-Treasury ratio stood at 85%, according to ICE.

The IHS Markit municipal analytics AAA curve showed short yields at 0.13% and 0.14% in 2021 and 2022, respectively, and the 10-year fell one basis point to 0.69% as the 30-year yield was unchanged at 1.41%.

Treasuries spiked as stocks rallied. The 10-year Treasury was yielding 0.93% and the 30-year Treasury was yielding 167%. The Dow rose 189 points, or 0.63%, the S&P 500 rose 1.14% and the Nasdaq rose 1.27%.