Lam Research Corp. reported stronger-than-expected 3Q results as revenues jumped 47% to $3.18 billion year-over-year and surpassed analysts’ expectations of $3.11 billion. The company’s top-line mainly benefited from increased demand for memory chips across personal computers, storage and networking categories driven by COVID-19 pandemic-led remote working and online learning trend.

Lam’s (LRCX) 1Q adjusted EPS spiked 78.3% to $5.67 year-on-year and beat Street estimates of $5.19. “Lam generated outstanding results in the September quarter with record revenues and earnings per share,” said Lam’s CEO Tim Archer. “Our strong operational execution is enabling the Company to meet our customers’ critical needs, providing a solid foundation to deliver on our long-term growth objectives.”

Lam expects 2Q revenues between $3.10 billion and $3.50 billion, which is above analysts’ projections of $3.08 billion. Adjusted EPS guidance range of $5.20-$6.00 compares with a Street consensus of $5.16. (See LRCX stock analysis on TipRanks).

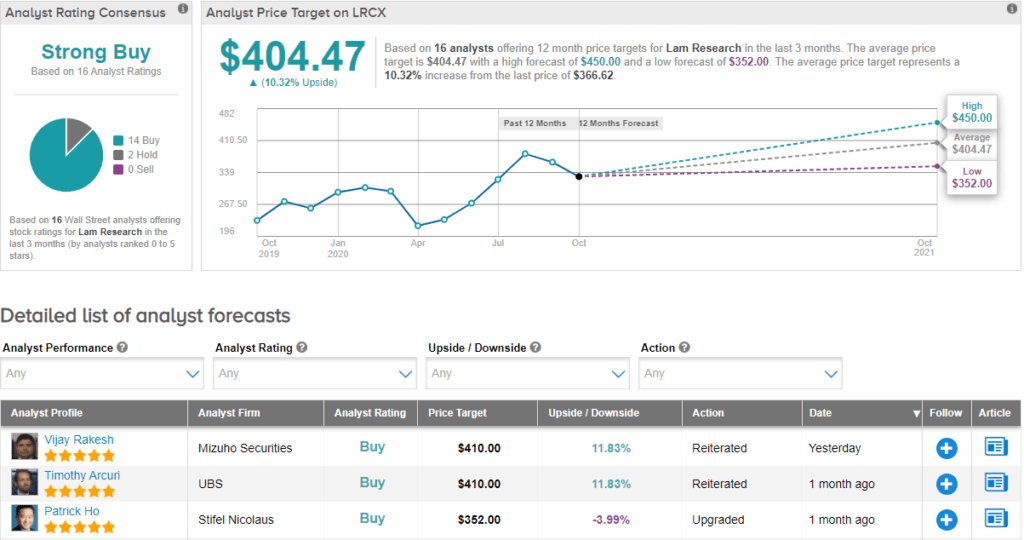

Following the company’s 2Q results, Mizuho Securities analyst Vijay Rakesh raised the stock’s price target to $410 (11.8% upside potential) from $400 and reiterated a Buy rating. In a note to investors, Rakesh wrote, “We believe LRCX’s leadership in Memory WFE (wafer fabrication equipment) (historical ~70% of rev) positions it well to benefit from increasing capital intensity of 3D-NAND and DRAM (dynamic random-access memory) 1y & 1z transitions.”

Currently, the Street is bullish on the stock. The Strong Buy analyst consensus is based on 14 Buys versus 2 Holds. With shares up over 25% year-to-date, the average price target of $404.47 implies further upside potential of about 10.3% to current levels.

Related News:

KeyCorp’s Profit Rises As Credit Loss Provisions Drop 20%

Pentair Raises 2020 Outlook As Pool Sales Rise; Shares Gain 4%

Albertsons Jumps 5.6% As Online Sales Pop 243%